Submitted by Gail Tverberg via Our Finite World blog,

$50 per barrel oil is clearly less impossible to live with than $30 per barrel oil, because most businesses cannot make a profit with $30 per barrel oil. But is $50 per barrel oil helpful?

I would argue that it really is not.

When oil was over $100 per barrel, human beings in many countries were getting the benefit of most of that high oil price:

- Some of the $100 per barrel goes as wages to the employees of the oil company who extracted the oil.

- Often, the oil company contracts with another company to do part of the oil extraction. Part of the $100 per barrel is paid as wages to employees of the subcontracting companies.

- An oil company buys many goods, such as steel pipe, which are made by others. Part of the $100 per barrel goes to employees of the companies making the goods that the oil company buys.

- An oil company pays taxes. These taxes are used to fund many programs, including new roads, schools, and transfer payments to the elderly and unemployed. Again, these funds go to actual people, as wages, or as transfer payments to people who cannot work.

- An oil company pays dividends to stockholders. Some of the stockholders are individuals; others are pension funds, insurance companies, and other companies. Pension funds use the dividends to make pension payments to individuals. Insurance companies use the dividends to make insurance premiums affordable. One way or another, these dividends act to create benefits for individuals.

- Interest payments on debt go to bondholders or to the bank making the loan. Pension plans and insurance companies often own the bonds. These interest payments go to pay pension payments of individuals or to help make insurance premiums more affordable.

- A company may have accumulated profits that are not paid out in dividends and taxes. Typically, they are reinvested in the company, allowing more people to have jobs. In some cases, the value of the stock may rise as well.

When the price falls from $100 per barrel to $50 per barrel, the incomes of many people are adversely affected. This is a huge negative with respect to world economic growth.

If the price of oil drops from $100 per barrel to $50 per barrel, this change adversely affects the income of a large share of people who formerly benefited from the high price. Thus, the drop in oil prices affects the incomes of many of the people listed in the previous section.

Furthermore, this drop in income tends to radiate outward to the rest of the economy because each worker who is laid off is forced to purchase fewer discretionary items. These workers are also less able to take on new debt, such as to buy a new car or house. In some cases, they may even default on existing debt.

A drop in oil prices from $100+ per barrel to $50 per barrel leads to job layoffs by oil companies and their subcontractors. Oil companies and their subcontractors may even reduce dividends to shareholders.

While oil prices have recently been as low as $30 per barrel, the subsequent rise in prices to $50 per barrel is not enough to start adding new production. Prices are still far too low to encourage new development.

In 2016, other commodities besides oil have a problem with price below the cost of production.

Many commodities, including coal and natural gas, are currently affected by low prices. So are many kinds of metals, and some kinds of food commodities. Thus, there is pressure in a wide range of industries to lay off workers. There are many parts of the world now feeling recessionary forces.

As prices fall, the pressure is for high-cost producers to drop out. As this happens, the world’s ability to make goods and services falls. The size of the world economy tends to shrink. This shrinkage is clearly not good for a world economy that needs to grow in order for investors to earn a profit, and in order for debtors to repay debt with interest.

Growing demand comes from a combination of increasing wages and increasing debt.

The recent drop in oil prices from the $100+ level seems to come from inadequate demand for oil. This is equivalent to saying that oil at such a high price has not been affordable for a significant share of buyers. We can understand what might have gone wrong, by thinking about how demand for oil might be increased.

Clearly, one way of increasing demand is through increased productivity of workers. If this increased productivity allows wages to rise, this increased productivity can cycle back through the economy as increased demand for goods and services. We can think of the process as an “economic growth pump” that allows continued economic growth.

Generally, increased productivity of workers reflects the use of more capital goods, such as machines, vehicles, and buildings. These capital goods are made using energy products, and operate using energy products. Thus, energy consumption is an important part of the economic growth pump. These capital goods are frequently financed using debt, so debt is another important part of the economic growth pump.

Even apart from the debt necessary for financing capital goods, another way of increasing demand is by adding more debt. If a company adds more debt, it can often hire more workers and can add to its holdings of property. These also help raise the output of the company. As long as the output that is added is sufficiently productive that it can repay the added debt with interest, adding more debt tends to enhance the workings of the economic growth pump.

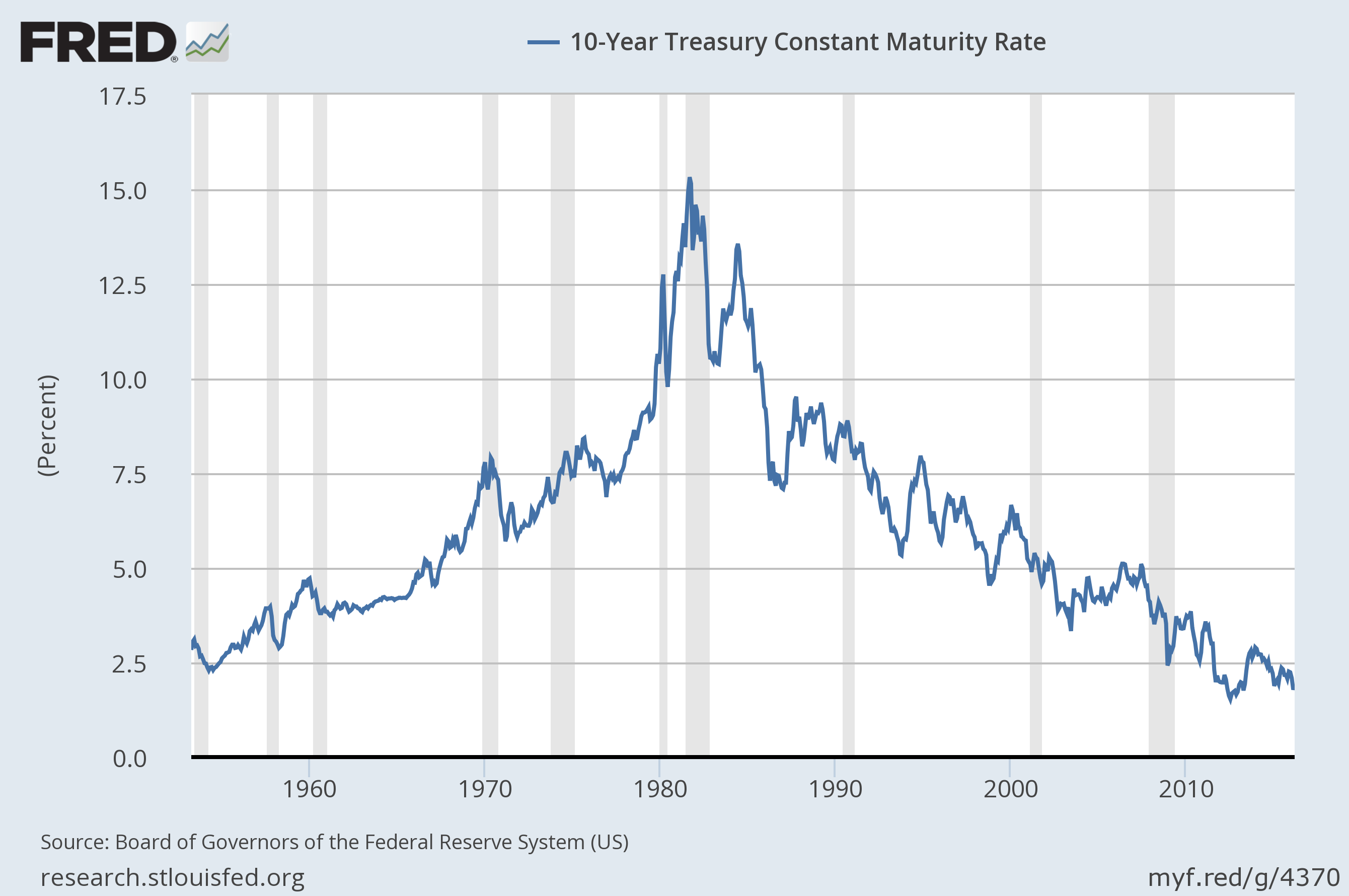

The way governments have attempted to encourage the use of increased debt in recent years is by decreasing interest rates. The reason this approach is used is because with a lower interest rate, a broader range of investments can seem to be profitable, after repaying debt with interest. Even very “iffy” investments, such as extraction of tight oil from the Bakken, can appear to be profitable.

The extent of the decrease in interest rates since 1981 has been amazingly large.

Figure 1. Ten year treasury interest rates, based on St. Louis Fed data.

Since 2008, additional steps have been taken to decrease interest rates even further. One of these is the use of Quantitative Easing. Another is the recent use of negative interest rates in Europe and Japan.

Falling demand would seem to suggest that the world’s economic growth pump is no longer working properly. This is happening, even with all of the post-1981 manipulations of interest rates to reduce the cost of borrowed capital, and thus reduce the required threshold for profitability of new investments.

What could cause the economic growth pump to stop working?

One possibility is that accumulated debt reaches too high a level, based on historical parameters. This seems to be happening now in many parts of the world.

Another thing that could go wrong is that the price of oil rises so high that capital goods based on oil are no longer cost effective for leveraging human labor. If this happens, manufacturing is likely to move to countries that use a cheaper mix of fuels, typically including more coal. The shift of manufacturing to China seems to reflect such a change.

A third thing that could go wrong is that pollution becomes too great a problem, forcing a country to slow down economic growth. This seems to be at least part of China’s current problem.

If oil prices drop from $100 to $50 per barrel, this has an adverse impact on debt levels.

With lower oil prices, workers are laid off, both from oil companies and from companies that provide goods and services to oil companies. These workers, in turn, are less able to take on new debt. In some cases, they may also default on their debt.

Oil companies with reduced cash flow are also less able to repay their debt. In some cases, companies may file for bankruptcy. The result is generally that existing debt is “written down.” Even if an oil company does not file for bankruptcy, it is likely to have difficulty adding new debt. The trend in the amount of debt outstanding is likely to change from increasing to decreasing.

As the amount of debt shifts from increasing to decreasing, the economy tends to shift from increasing to shrinking. Instead of adding more employees, companies tend to reduce the number of employees. If many commodities are affected, the impact can be very large.

We need oil prices to rise to $120 per barrel or more.

The current price of $50 per barrel is still way too low. A post I published in February 2014 was called Beginning of the End? Oil Companies Cut Back on Spending. In it, I talked about an analysis by Steve Kopits of Douglas-Westwood. In this analysis, Kopits points out that even at that time–which was before oil prices began dropping in mid-2014–major oil companies were beginning to cut back on spending for new production. Their cost of production was at that time typically at least $120 or $130 per barrel, if prices were to be high enough so that companies could fund new development without adding huge amounts of new debt. Oil prices could perhaps be lower if oil companies could fund their operations using large increases in debt. Company management recognized that such a funding approach would not be prudent–it could lead to unmanageable debt levels.

Today’s cost of oil production is likely to be even higher than it was when Kopits’ analysis was performed in early 2014. If we expect oil production to continue to rise, we probably need oil prices in the $120 to $150 per barrel range for several years. Prices at such a level are likely to be way too high for consumers, because wages do not rise at the same time as oil prices. Consumers find that they need to cut back on discretionary expenditures. These spending cutbacks tend to lead to recession and falling oil prices.

We can think of our economy as being like a big ball, which can be pumped up to greater and greater size with either rising productivity or rising debt.

This process can continue to work, only as long as the debt added is sufficiently productive that it is possible to repay the debt with interest. We seem to be reaching the end of the line on this process. Returns keep falling lower and lower, necessitating ever-lower interest rates.

To some extent, the pumping up of oil prices that occurs in this process represents a lie, because the energy content of a barrel of oil remains unchanged, regardless of price. In fact, the energy of coal and of natural gas per unit of production remains unchanged as well. The value of energy products to society is determined by their physical ability to leverage human labor–for example, how far diesel oil can move a truck. This ability is unchanged, regardless of how expensive that oil is to produce. This is why, at some point, we find that high-priced energy products simply don’t work in the economy. If we spend the huge amount of resources required for the production of energy products, we don’t have enough resources left over for the rest of the economy to grow.

Low oil prices, plus low commodity prices of other kinds, seem to indicate that we are reaching the end of the line in the “pump up the economy with debt” approach. We have been using this approach since 1981. At this point, we have no idea what economy growth would look like, without the stimulus of falling interest rates.

The drop in oil prices and other commodity prices since mid-2014 seems to represent a “shrinking back” of our ability to use debt to raise prices to a level sufficient to cover the cost of extraction, plus associated overhead costs, including taxes. This drop in prices should be an alarm bell that something is seriously wrong. Without continuously rising prices, to keep up with ever-rising extraction costs, fossil fuel production will at some point come to a halt. Renewables will not work well either, because prices will not be high enough for them to be competitive.

Of course, once the economy stops growing, the huge amount of debt we have amassed becomes un-payable. The whole system we have built will begin to look more and more like a Ponzi Scheme.

We are blind to the possibility that oil prices of $50 per barrel may indicate that we are reaching “the end of the line.”

The popular belief is that everything will work out fine. Oil prices will rise a bit, and somehow the economy will get along with less fossil fuel. Somehow, we will make it through this bottleneck.

If we would study history, we would discover that there have been many situations of overshoot and collapse. In fact, those situations tend to look quite a bit like the situation we are seeing today:

- Falling resources per capita, because of rising population or exhaustion of resources

- Falling wages of non-elite workers; greater wage disparity

- Governments finding it increasingly difficult to fund needed programs

There is a popular belief that oil prices will rise, if there is a shortage of energy products. In prior collapses, it is not at all clear that prices have risen. We know that when ancient Babylon collapsed, demand for all products, even slaves, fell. If we are reaching collapse now, we should not be surprised if the prices of commodities, including oil, stay low. Alternatively, they might spike, but only briefly—not enough to really fix our current situation.

Too many wrong theories

Part of our problem is too much confidence that the “magic hand” of supply and demand will fix the economy. We don’t really understand how demand is tied into affordability, and how affordability is tied into wages and debt. We don’t realize that the view that oil prices can rise endlessly is more or less equivalent to the view that economic growth can continue indefinitely in a finite world.

Another part of our problem is failure to understand how the economic pump that keeps the economy operating works. Once debt rises too high, or the cost of energy extraction rises too high, we can no longer keep the system going. Price tends to fall below the cost of energy extraction. The quantity of energy products consumed cannot rise fast enough to keep the economic growth pump operating.

Clearly neoclassical economics doesn’t properly model how the economy really works. But the Energy Returned on Energy Invested (EROEI) theory of Biophysical Economics does not model the current situation well, either. EROEI theory is generally focused on the ratio of Energy Returned by some alternative energy device to Fossil Fuel Energy Used by the same alternative energy device. This focus misses several important points:

- The quantity of energy consumed by the economy needs to keep rising, if human productivity is to keep growing, and thus allow the economy to avoid collapsing. EROEI calculations normally have little to say about the quantity of energy products.

- The quantity of debt required to produce a given amount of energy by an alternative energy device is very important. The more debt that is added, the worse the alternative energy device is for the economy.

- In order for the economic growth pump to keep working, the return on human labor needs to keep rising. This is equivalent to a need for the wages of non-elite workers to keep rising. This is a requirement relating to a different kind of EROEI—energy return on human labor, leveraged with various types of supplemental energy. Today’s EROEI theorists tend to overlook this type of EROEI.

EROEI theory is a simplification that misses several important parts of the story. While a high fossil fuel EROEI is necessary for an alternative to substitute for fossil fuels, it is not sufficient. Thus, EROEI analysis tends to produce “false favorable” results.

Lining up resources in order by their EROEIs seems to be a useful exercise, but, in fact, the cut-off likely needs to be higher than most have supposed, in order to keep total costs low enough so that the economy can really afford a given energy source. In addition, resources that add heavily to debt requirements are probably unhelpful, regardless of their calculated EROEIs.

Conclusion

We are certainly at a worrying point in history. Our networked economy is more complex than most researchers have considered possible. We seem to be headed for collapse because of low prices, rather than high. The base scenario of the 1972 book “The Limits to Growth,” by Donella Meadows and others, seems to indicate that the world will likely reach limits about the current decade.

The modeling done in 1972 laid out the basic situation, but could not be expected to explain precisely how collapse would occur. Now that we are reaching the expected timeframe, we can see more clearly what seems to be happening. We need to be examining what is really happening, rather than tying ourselves to outdated ideas of how the economic system works, and thus, what symptoms we should expect as we approach limits. It may be that $50 per barrel oil is one of the signs that collapse is not far away.

The post $50 Oil Doesn’t Work appeared first on crude-oil.top.