After the Monday Mayhem from the Turkey contagion, a sense of calm descended on FX markets during today’s Asian session. USD/TRY headed lower from its record high yesterday as the markets digested the impact and effectiveness of the central bank’s measures announced yesterday.

Selling of emerging currencies eases

The move in USD/TRY prompted other emerging currencies to stage a bit of a comeback against the US dollar with USD/ZAR dropping 8.4%, USD/MXN 2.7% and USD/INR 0.75%. EUR/USD also benefited from the US dollar’s retreat, rising 0.16% to regain the 1.14 handle. Equity markets also had a respite, with the Nikkei225 gaining 1.23%, Australian shares rose 0.66% while the Singapore30 added 0.54%. The only black spot was China where disappointing data knocked 0.51% off the index.

EUR/USD Daily Chart

Source: Oanda fxTRade

China data disappoints

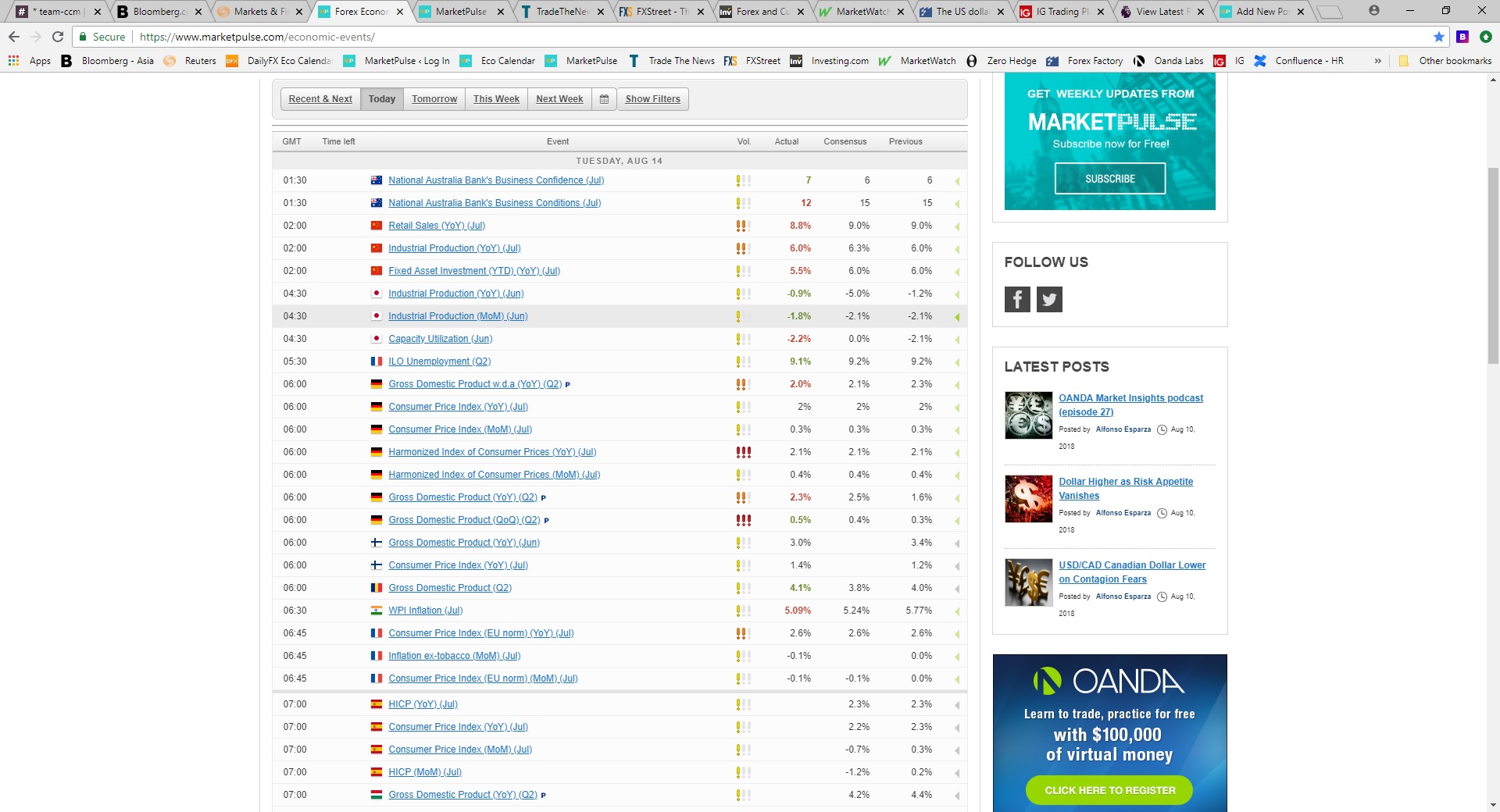

China released a set of second-tier data for July today and each data point came in below expectations. Retail sales grew 8.8% y/y after 9% growth in June and missed analysts’ expectations of steady 9% growth again. Industrial production held steady at +6.0% y/y though was also mellow forecasts of an increase of 6.3% while fixed asset investment missed with 5.5% annual growth versus expectations of a 6.0% gain. The jobless rate rose to 5.1% in July from 4.8% but Chinese officials were quick to point out that this was due mainly to seasonal factors.

Officials also commented that the other data pointed to a steady economy even though the domestic and international environment had become tricky with the effects of global trade tensions starting to show up in the global economy.

Australia’s second-tier data was mixed with the NAB business conditions index sliding to 12 in July from 15 in June though the more forward-looking confidence index improved a notch to 7 from 6. The Aussie has move higher on the day though this is more likely due to the US dollar’s dip rather than anything from the data.

Source: MarketPulse

The full data calendar can be viewed at https://www.marketpulse.com/economic-events/

Euro-zone Q2 GDP revision on tap

There is not much of an expectation for Euro-zone Q2 GDP to be revised from the provisional reading of +0.3% q/q and +2.1% y/y. That said, industrial production could show a contraction of 0.4% m/m in July, according to economists’ forecasts. From Germany we can expect ZEW sentiment surveys which have been generally trending lower over the past six months while the UK releases unemployment and average earnings data. The US data calendar is relatively mundane with export/import prices followed by the weekly API crude inventories.

OANDA Market Beat: Risk Aversion Boosts Dollar

Source: Oanda MarketPulse