![]()

![]()

![]()

Markets back in the red

The usual Monday morning sell-off has been less severe than we’ve seen in recent weeks, although Europe has been moving deeper into the red in early trade after a relatively unchanged open so that may change quickly.

Source – Thomson Reuters Eikon

Asia wasn’t so lucky but then, there was some catch up to be had following another sharp decline in Europe and the US on Friday. The losses are pretty modest by recent standards as well so investors may even be a little encouraged, depending on how the rest of the day goes in Europe and the US.

The news over the weekend was no more pleasant, with the death count nearing 34,000, up almost 7,000 since Friday. Italy will be hoping that two consecutive days of fewer deaths is cause for optimism, although it may be cautious optimism following last week’s false dawn.

The raft of global stimulus measures continued on Monday, with the People’s Bank of China cutting the reverse repo rate by 20 basis points, Monetary Authority of Singapore lowering the midpoint of the currency band and Australia preparing to commit to $80 billion of spending over the next six months which includes wages subsidies.

As we’ve seen already though, these measures aren’t having the same impact in the market as they have in the past. While they may soften the blow of any downturn, they stand no chance of preventing it altogether and a global recession is coming. The hope though is that these measures will ensure it is as brief as possible and maybe even turbo charge the recovery.

Unfortunately, we’re still reliant on measures to contain the coronavirus actually working and as Italy is finding, this is not straight forward. Last week’s huge stimulus measures in the US provided some reprieve for markets and investors will be encouraged by the start on Monday but I’m far from convinced that we’ve seen the bottom yet.

Oil dips below $20 as oil price war shows no sign of ending

Oil prices have had another woeful start to the week, with WTI dipping briefly below $20 a barrel and Brent nearing $23, its lowest point since late 2002. These really are extraordinary times. Saudi Arabia and Russia appear to closer to ending the price war which has hugely exacerbated the supply/demand problem in these already troubling times.

The victims of the war will likely be elsewhere though, with US shale expected to come under considerable pressure. The US is still pumping near-record amounts of crude but the late oil rig data suggests that may not last much longer. It’s been on a downward trend for a while now but last week’s plunge was quite significant.

WTI Daily Chart

OANDA fxTrade Advanced Charting Platform

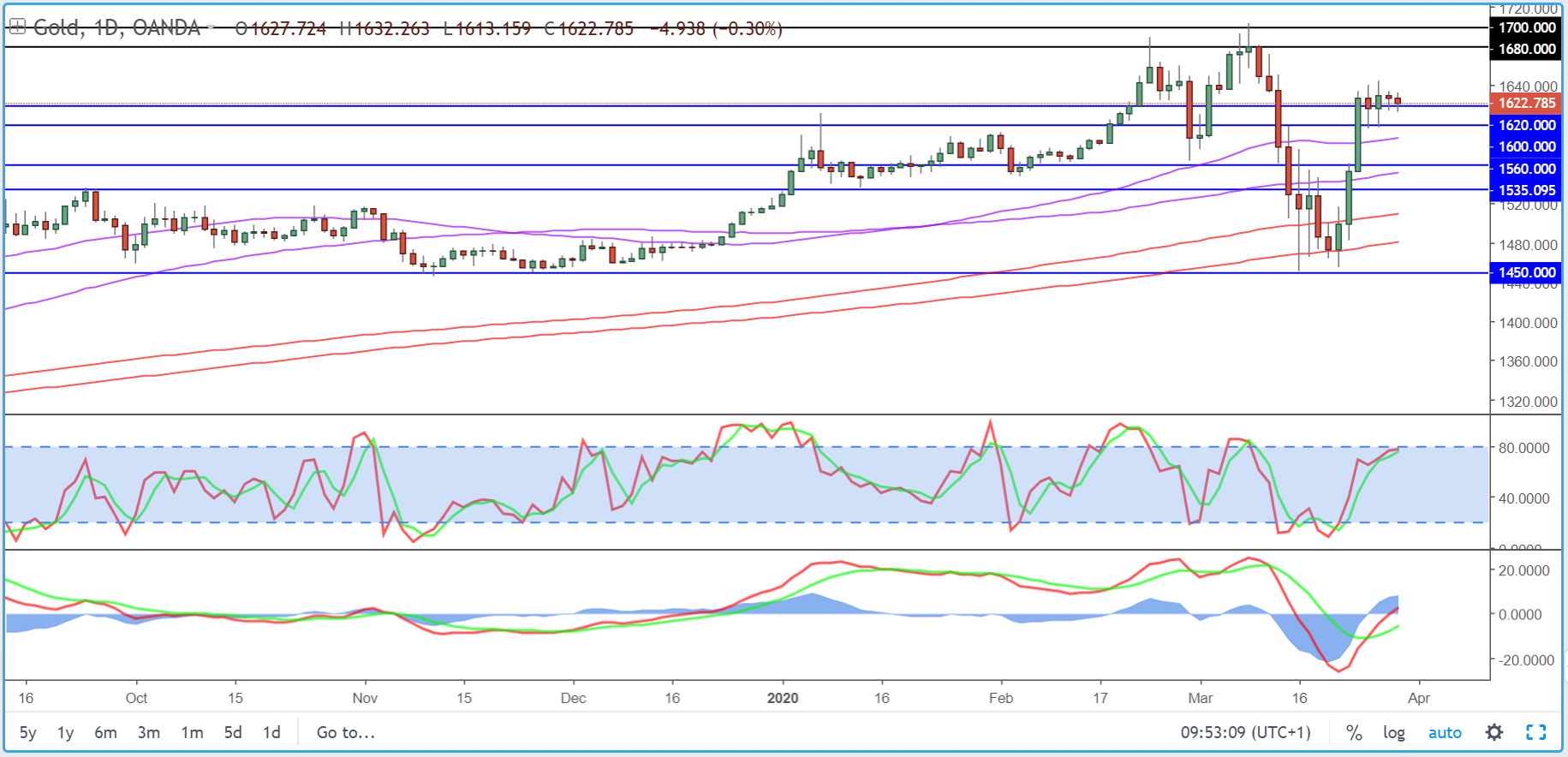

Gold vulnerability undermines rally

Gold is relatively stable this morning, seemingly having found its feet in the $1,600-1,640 range. While I don’t doubt its long-term safe haven credentials, this is still a market prone to sharp sell-off’s which continue to negatively impact gold. This will continue to undermine its bullish case even if it wouldn’t be in doubt in normal times.

Gold Daily Chart

Bitcoin fails at $7,000

Bitcoin took a hit over the weekend despite having been on a steady bullish trajectory in recent weeks. The $7,000 level proved a step too far, despite numerous attempts and the cryptocurrency has this morning dipped back below $6,000. The broader risk reversal over the last couple of sessions won’t help matters and could keep cryptos under pressure.

Bitcoin Daily Chart

Source – Thomson Reuters Eikon

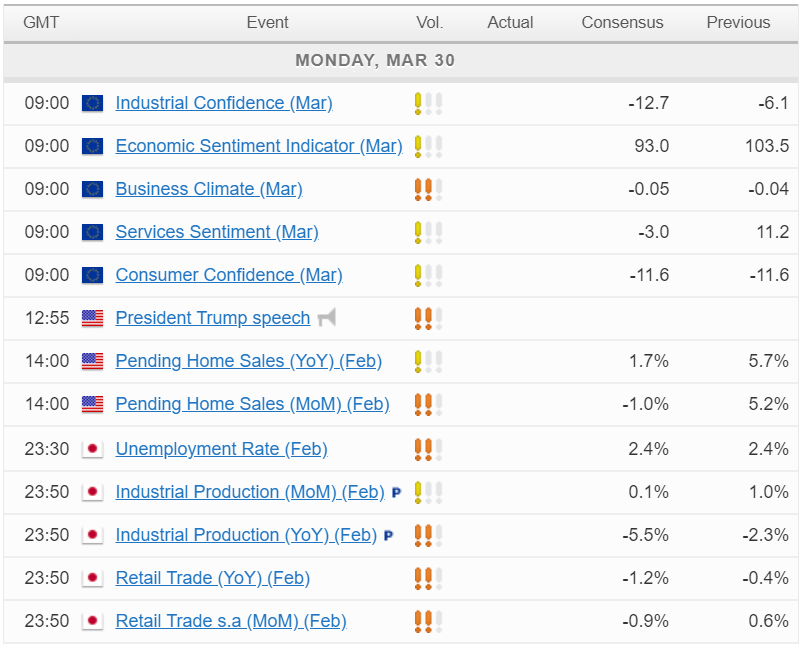

Economic Calendar

For a look at all of today’s economic events, check out our economic calendar.