Monday October 15: Five things the markets are talking about

Following a weekend of warnings on global economic fragility from G10 finance leaders at an IMF meeting in Bali, has global equities starting this new week on the back foot, with regional bourses in Asia and Europe seeing red, while U.S equity futures are pointing to deep declines.

Sovereign yields are lower in this cautious climate, while yen has pushed higher along with gold. Crude oil has advanced as tensions rise between the U.S and Saudi Arabia over a missing journalist.

Politics and data are never a good mix and this week is awash with both.

Italy is to submit its contentious budget to the E.C. Already; the proposed budget has potentially broken specific thresholds, which would require a lot of debating from both parties. Expect Italian BTP yields again to come under pressure, backing up towards the psychological +4%.

The E.U meets on Wednesday and will get an update on the status of negotiations with the U.K’s Brexit. Expect the Irish border to be the ‘hot topic du jour. If there is insufficient progress, the possibility of a special summit next month to finalize an agreement looks dead in the water. Dealers expect the pound to remain volatile in the short-term.

The U.S Treasury report about the international economy and the FX market is to be released Tuesday. To neutral observers, China does not meet the threshold of “manipulation.” However, Trumps interpretation may be very different.

On the data front, the U.S releases retail sales this morning (08:30 am EDT) and FOMC minutes on Wednesday.

Across the pond, the U.K presents its labour report tomorrow, (Oct 16) inflation Wednesday (Oct 17) and retail sales Thursday (Oct 18).

In Canada, Friday’s upcoming data includes retail sales, and CPI – neither of the reports are expected to dissuade the market of pricing in a +25 bps rate hike at next weeks Bank of Canada (BoC) monetary policy decision.

1. Equities see red

In Japan overnight, the Nikkei closed at a two month low as automakers and other manufacturers were hit by news that the Trump administration would seek a provision about currency manipulation in future trade deals. The Nikkei share average ended down -1.8%, the weakest closing point since mid-Aug, while the broader Topix dropped -1.6%, the lowest close in seven-months.

Down-under, the ASX 200 fell to a six-month low overnight, led by the banking sectors growing concerns about the hit to earnings from an inquiry into misconduct. The S&P/ASX 200 index fell -1%. In S. Korea, the Kospi stock index fell -0.77% as institutions cut their exposure to riskier assets. The country’s biggest automaker Hyundai Motor slipped -1.7%, marking its lowest trading level in eight-years.

In China and Hong Kong, stock markets again slipped overnight following last week’s deepest dive in eight-months, as investors await the latest twist in the Sino-U.S trade dispute. The Shanghai Composite index closed lower by -1.5%, while in Hong Kong the Hang Seng closed -1.4% lower.

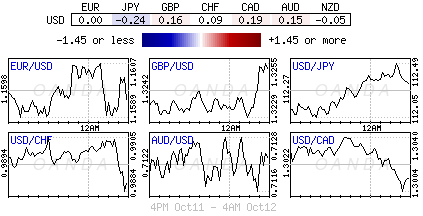

In Europe, regional bourses trade lower across the board, tracking U.S futures and Asian indices lower. The FTSE and sterling (£1.3140) trade a tad lower after the E.U and U.K paused Brexit talks until after this week’s mini-summit.

U.S stocks are set to open deep in the ‘red’ (-0.8%).

Indices: Stoxx600 -0.6% at 356.8, FTSE -0.3% at 6976, DAX -0.4% at 11474, CAC-40 -0.6% at 5066, IBEX-35 -0.3% at 8876, FTSE MIB -0.2% at 19225, SMI % at -0.8%, S&P 500 Futures -0.8%

2. Oil prices rise on Saudi tensions, gold higher

Oil prices remain bid this Monday morning as tension over the disappearance of a Washington post journalist and Saudi critic, Jamal Khashoggi, fuelled supply worries, although concerns over the long-term demand outlook dragged on sentiment.

Brent crude oil jumped +$1.49 a barrel to a high of +$81.92 before easing to +$81.13, up +70c. U.S crude (WTI) was last up +40c at +$71.74.

Saudi Arabia has been under pressure since Khashoggi, a U.S. resident, disappeared on Oct. 2 after visiting the Saudi consulate in Istanbul.

President Trump has threatened “severe punishment” if it is found that the journalist was killed in the consulate.

On Sunday, the Saudi’s said it would retaliate to any action taken against them over the Khashoggi case. The market is tentatively concerned that the Saudis may use oil as a tool for retaliation.

Despite prices starting the week better bid, there are still lower that last week’s high print.

Also limiting price gains is a report from the IEF last Friday stating that the market looked “adequately supplied for now” and cut its forecasts for world oil demand growth this year and next.

Ahead of the U.S open, gold prices have jumped +1% to hit a three-month high as global stocks resumed their fall and investors wrestled with the impact of the ongoing Sino-U.S. trade war and higher U.S interest rates. Spot gold is up +0.9% at +$1,228.24 an ounce, while U.S gold futures are up +0.8% at +$1,231.80 an ounce.

3. Italian and Portugal yields fall

Portuguese and Italian government bond yields have fallen this morning, with prices outperforming euro zone peers after ratings agency Moody’s upgraded Portugal’s credit rating back to investment grade.

Portugal’s 10-year bond yield fell -4 bps to +2.01% after Moody’s lifted its credit rating to Baa3 on Friday.

The positive periphery sentiment from Portugal has spilled over into Italy’s battered bond market. Italian 10-year BTP yields are down -4.5 bps to +3.53%.

Note: Expect Italian yields to trade rather volatile this week as Italy presents its budget to the E.C.

Elsewhere, the yield on U.S 10’s fell -1 bps to +3.15%. In Germany, the 10-year Bund yield has dipped -1 bps to +0.49%, the lowest in more than a week. In the U.K, the 10-year Gilt yield has eased -2 bps to +1.614%, the lowest in more than a week.

4. Dollar’s safe haven flows ease

Risk aversion flows initially provided a bid for the traditional safe-haven currencies of JPY (¥111.75) and ‘big’ USD, however, market sentiment has eased a tad ahead of the U.S open.

GBP (£1.3147) opened below the psychological £1.31 handle on concerns that a Brexit agreement might be slipping away after the U.K and E.U negotiators were said to have called ‘a pause’ in their Brexit talks and would now wait for the outcome of a summit mid-week (Wed) before any resumption.

TRY ($5.8208) is firmer by over +1% outright for its seventh session gain on optimism that relations between Turkey and U.S would improve following the release of U.S Pastor Brunson.

Bitcoin prices have spiked +6.5% this morning, jumping above +$6,600. While the catalyst behind the move higher is not clear and with few ready to label bitcoin a “true store of value” in turbulent times, BTC has held up better than most of late.

5. Embarrassing losses in Bavarian election shake Merkel’s coalition

Germany’s grand coalition could become even further unstable after coalition members suffered humiliating results in an election in the southern state of Bavaria.

Chancellor Merkel’s Bavarian allies slumped to their worst election results in almost 70 years and her junior coalition partners, the center-left Social Democrats (SPD), saw support in Bavaria halved.

The SPD had hoped that infighting over immigration between Merkel’s Christian Democrats (CDU) and the Bavarian Christian Social Union (CDU) allies would give them a boost in Bavaria.

But instead, the party saw support fall to just under +10%, prompting a discussion over the sustainability of its alliance with Merkel’s conservatives at the national level.

Note: SPD members are still bitter over their leaders’ decision to join a Merkel-led government.

Merkel’s authority may be called into question as soon as in two-weeks in an election in the western state of Hesse – the state is ruled by Merkel’s CDU in a coalition with the Greens, but polls suggest she is losing further support.