Submitted by Lance Roberts via RealInvestmentAdvice.com,

After more than a week following the election, the markets, and a large chunk of the nation, remain a mixed bagged of emotions ranging from exuberance and disbelief to anger and depression. While I don’t want to get into the “left versus right” debate in this missive, it has been interesting to watch market participants swing from “Trump The Terrible” to “Trump The Great” in relation to the markets and economy and he isn’t even in office yet. It is the same as giving Obama the Nobel Peace Prize when he entered office, an action the Nobel committee has come to regret.

But which is it really?

While Trump certainly has an extensive list of actions for his first 100-days, there are many headwinds to actual policy implementation and ultimately their success. Also, a big part of the success of any policy comes down to one thing – “timing.” A good example of this is the “infrastructure spending” plans which will require a significant increase in the national debt to accomplish.

While the market participants have already been chasing financial and infrastructure related assets, an infrastructure program should be prepared but not implemented until the next recessionary drag in the economy. The debt increase needed to fund an infrastructure program, which would likely coincide with a new QE program to buy the debt, would potentially have the greatest effect at limiting the economic drag of the recession.

It is the same with trade policies, immigration reform and even tariffs. For every policy, there is a significant potential for a near-term negative impact on economic growth even though the long-run outcome will be positive. With an economy running at below 2%, consumers already heavily indebted, wage growth weak for the bulk of American’s, there is not a lot of wiggle room for policy mistakes.

Combine weak economics with higher interest rates, which negatively impacts consumption, and a stronger dollar, which weighs on exports, and you have a real potential of a recession occurring sooner rather than later.

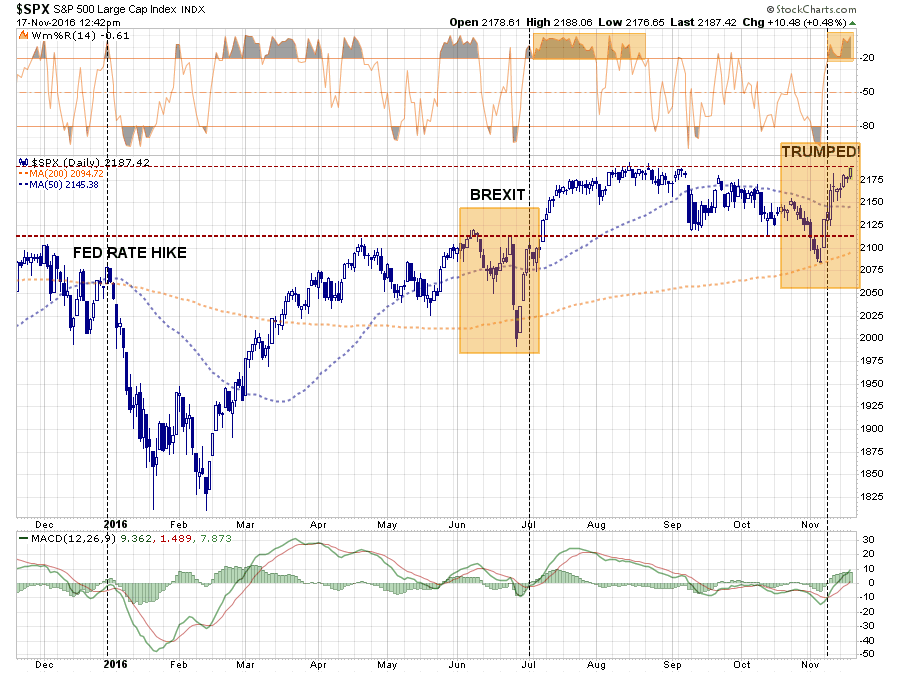

However, that is a conversation for later, as the flood of liquidity to support the markets once again, as was seen post the “Brexit” vote has propelled markets higher in a short-covering feeding frenzy. The chart below notes the similarities between the two events. A sharp sell-off to oversold conditions, a reflexive rally that potentially hits new highs, and then fizzles out.

Importantly, with next week being a light trading week, it would not be surprising to see markets drift higher. However, expect a decline during the first couple of weeks of December as mutual funds and hedge funds deal with distributions and redemptions. That draw down, as seen in early last December, ran right into the Fed rate hike that set up the sharp January decline.

With much of the same backdrop currently in the works, some caution is advised.

In the meantime, here is what I am reading this weekend.

Trumped! / Fed / Economy

- 2-Types Of Inflation: The Good & Bad by Danielle DiMartino-Booth via Money Strong

- What Adds Up & Doesn’t In Trump’s Plans by Lee Ohanian via San Francisco Chronicle

- Trumponomics Vs. Reality by Martin Feldstein via WSJ

- Paul Krugman Doubles Down On Fantasy by Steil & Smith via Council On Foreign Relations

- Coming To Terms With Trumponomics by John Cassidy via The New Yorker

- Yes, Trump Will Create Growth & Jobs by Stephen Moore via IBD

- Trump’s Next Default Lies Ahead by Brett Arends via MarketWatch

- Good Chance Trumped Handed A Recession by Chris Isidore via CNN Money

- The Trouble With Trump’s Infrastructure Plan by Tyler Cowen via Bloomberg

- Economic Doctors Misdiagnosed Economy by Ray Keating via Real Clear Markets

- Financial Crises & Policy Responses by Robert Litan via AEI

- I Can’t Believe What Just Happened by Paul Krugman via NYT

- Trump’s Impossible Economic Mission by Robert Samuelson via RCM

- Fed Ready For A Reckoning by Binyamin Appelbaum via NYT

- Who’s Going To Pay From Trump’s Plans by Marc Joffe via The Fiscal Times

Markets

- Is The Bull Market In Bonds Really Over? by Caroline Baum via MarketWatch

- 5 Reasons Investors Should Worry About Trump by Joachim Fels via MarketWatch

- Dividend Cuts Ramp Up by Ironman via Political Calculations

- Embrace Contrarian Thinking by Doug Kass via Real Clear Markets

- Don’t Believe The Great Great Bond Fake-Out by Jeff Reeves via MarketWatch

- Trumpageddon to Trumptopia! What’s Next? by Michael O’Rourke via HedgEye

- Market’s Two Bullish Arguments by Michael Kahn via Barron’s

- Trump-Rally Sits Atop A Lot Of “If’s” & “Maybe’s” by James Saft via Reuters

- Watch The Rise Of The Dollar by Jeffrey Snider via Alhambra Partners

- Trump Trade Is Getting Out Of Hand by James Mackintosh via WSJ

- Clear & Present Danger via Market Anthropology

- End Of The Year Rally? by Adam Shell via USA Today

Interesting Reads

- Populism Takes A Wrong Turn by Bill Gross via Janus Capital

- 2826 Day Old Bull Market A Headache by Joseph Ciolli via Bloomberg

- Trump Rally – Too Far Too Fast? by Paul La Monica via CNN Money

- Goldman Kills The Reflation Trade by Tyler Durden via ZeroHedge

- Rates Will Remain Low by David Trainer via Forbes

- Trump vs Rates by Mohamed El-Erian via Bloomberg

- If You Build It (Infrastructure), They Won’t Come by Stephen Entin via IBD

- A CasP Model Of The Stock Market by The Bichler & Nitzan Archives

- Oops! Single Family Permits Fall Flat by Aaron Layman via AaronLayman.com

- Judging Economic Policy by John Hussman via Hussman Funds

- Breadth Thrust To Launch Stocks Higher? by Dana Lyons via Tumblr

- Just One Question For Yellen by Jesse Felder via The Felder Report

“I like thinking big. If you’re going to be thinking anything, you might as well think big.” — Donald Trump

The post Weekend Reading: The Trump Effect appeared first on crude-oil.top.