Submitted by Charles Hugh-Smith via OfTwoMinds blog,

The fallacy in this assumption is that homeowners' incomes do not automatically rise along with housing valuations.

In my recent entry Dear Homeowner: If You're Paying $260,000 in Property Taxes Over 20 Years, What Exactly Do You "Own"?, I questioned the consequences of high property taxes. Some readers wondered if I was saying all property taxes should be abolished. The short answer is no–what I was questioning is local government reliance on property taxes to the point that owning a home no longer makes financial sense because the property taxes consume any appreciation other than the transitory "wealth" generated by a housing bubble.

In effect, local tax authorities are capturing all future appreciation for themselves. Note that applies to areas with high property taxes–in excess of $10,000 annually, not locales with annual property taxes of $2,000.

State and local taxes–sales, income and property–tax very different events. Sales taxes are based on consumption, and are typically highly regressive, as low-income households pay a higher percentage of their income on sales taxes than higher-income households.

Income taxes are typically progressive, as the higher one's income, the more income tax one pays.

Property tax is not based on consumption or income, but on the presumed wealth and income of property owners. In effect, property taxes are a wealth tax: if you can afford a house, you can afford property taxes.

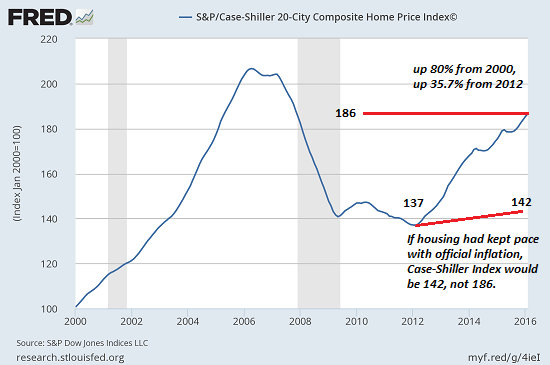

The fallacy in this assumption is that homeowners' incomes do not automatically rise along with housing valuations. Consider the 35% increase in the Case-Shiller 20-City Index since 2012: in a four-year period that officially experienced a mere 4% inflation, housing leaped 35%.

Meanwhile, real median household incomes rose a paltry 5%. Local tax authorities love housing bubbles because rising valuations justify higher property taxes. But the homeowners' income needed to pay higher property taxes may well have declined during the bubble due to layoffs, shortened hours, medical emergency, reduced bonus, etc.

Real estate professional EB described the consequences of this mismatch of earnings need to pay property taxes and soaring property taxes:

You are correct that property taxes are an oft-forgotten cost of homeownership that many buyers fail to properly evaluate when determining how much house they can afford over the long term.

Perhaps a better way to view property taxes is as an inefficient proxy for income taxes — state and local governments assuming that people who can afford a home of a certain value, must have sufficient income to pay ad valorem taxes and per foot and per parcel charges at a given rate.

In a volatile economy, that assumption is often invalid. When the Fed runs out of monetary games to play, and asset values across the economy normalize, both state and local governments and homeowners will all be in a pinch — governments because the valuation-based portion of the tax base will crash, and homeowners because the fixed charges will no longer fit within their diminished incomes.

This is already occurring in suburban Chicago, where annual property taxes can approach 10% (!) of property values.

In a recession, earnings can decline very quickly indeed. Meanwhile, property taxes are "sticky": they only decline grudgingly (if ever), and only if homeowners pursue bureaucratic appeals based on the declining value of their home.

Owning your house free and clear (no mortgage) is no guarantee you'll be able to live there once property taxes are $1,000 per month. One of the emotional triggers of Prop 13 limitations on property tax increases in California was the stories of elderly pensioners having to sell their homes because they could no longer afford the skyrocketing property taxes.

A wealth tax based on housing valuations applies equally to homeowners with diminishing income, i.e. the decidedly non-wealthy.

As pensions dry up and blow away under the relentless erosion of the Federal Reserve's zero-interest rate policy (ZIRP), unaffordable property taxes may well start evicting homeowners from the "asset" they mistakenly thought they "owned." If your Social Security pension can barely pay your property tax, never mind your Medicare, healthcare costs, food and other living expenses, then what exactly do you own?

As I noted before, as far as the tax authorities are concerned, all you really own is an obligation to pay property taxes and an option to profit from the next housing bubble. If the bubble pops in a recession that also costs you your job, well tough luck, Bucko–your "asset" reverts to the state/county as payment for property taxes you can't possibly pay.

If politicos and tax authorities think people will passively watch their neighbors lose their homes to sky-high property taxes, they will soon discover their mistake.

My new book is #3 on Kindle short reads -> politics and social science: Why Our Status Quo Failed and Is Beyond Reform ($3.95 Kindle ebook, $8.95 print edition) For more, please visit the book's website.

The post Are Property Taxes A “Wealth Tax” On The (Mostly) Non-Wealthy? appeared first on crude-oil.top.