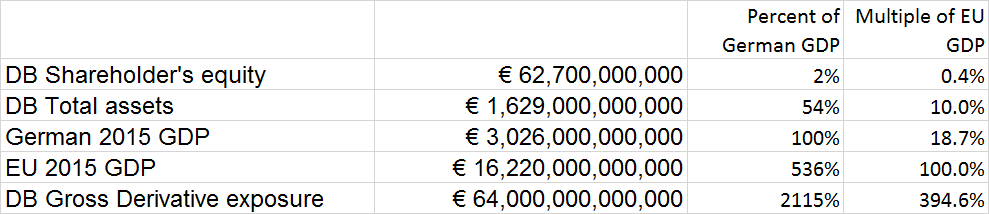

I was discussing the US Department of Justice $14B fine levied at Deutsche Bank with my 15 year old son last week. I told him the fine amounted to roughly 70% of Deutsche’s market cap, while a similar retroactive tax levy from the EU towards Apple for $14B was about 3% of their cash on hand or a quarter’s operating profit. My son said, “Whoah! Waitaminute! I thought Deutsche Bank was a big company like Apple. Didn’t you say that they had trillions of euros of assets on their balance sheet?”.

Indeed, I did say such, and he brings up a very valid point that is missed by many a so-called professional. DB is valued at 14.5 billion euros by Mrs Market, yet that amount controlls 1.8 trillion euros worth of assets, and 1.415 trillion after netting and credit adjustments, etc. And to think, some people think a 90 LTV loan is pushing the leverate limiit. Let’s take a look at this from a graphica perspective to illustrate just how absurd it is…

Over time, the accounting expression of equity diverges significantly from the markets perception of the bank’s equity value. Somebody is most assuredly mistaken! As of today, DB’s books are carrying equity value at 3x that of the stock market.

If one were to use the stock market’s equity valuation, one would see that a very, very tiny sliver of equity is controlling nearly 1.5 trillion euro of assets – and that’s after the slimming down game is done. Expressed differently, DB is leveaged 97.4x.

For those who feel this is an unrealistice way of looking at things, run the same exercise for every failed bank and cross reference the results to that of the European banking regulatory body’s methodology of calculating leverage and tell me which methid was (and is) the better predictor of bank failure.

| Leverage ratio measures | ||||||||||

| (In EUR bn., unless stated otherwise) | Dec 31, 2014 | Mar 31, 2015 | Jun 30, 2015 | Sep 30, 2015 | Dec 31, 2015 | Mar 31, 2016 | Jun 30, 2016 | Sep 28, 2016 | ||

| Total assets | 1,709 | 1,955 | 1,694 | 1,719 | 1,629 | 1,741 | 1,803 | 1,803 | ||

| Changes from IFRS to CRR/CRD41 | (264) | (407) | (233) | (299) | (234) | (350) |

|

|

||

| Derivatives netting1 | (562) | (668) | (480) | (508) | (460) | (523) | (556) | (556) | ||

| Derivatives add-on1 | 221 | 227 | 198 | 177 | 166 | 157 | 157 | 157 | ||

| Written credit derivatives1 | 65 | 58 | 45 | 42 | 30 | 31 | 24 | 24 | ||

| Securities Financing Transactions1 | 16 | 20 | 21 | 22 | 25 | 25 | 35 | 35 | ||

| Off-balance sheet exposure after application of credit conversion factors1 | 127 | 134 | 131 | 109 | 109 | 102 | 102 | 102 | ||

| Consolidation, regulatory and other adjustments1 | (131) | (177) | (148) | (140) | (104) | (140) | (151) | (151) | ||

| CRR/CRD4 leverage exposure measure (spot value at reporting date)1 | 1,445 | 1,549 | 1,461 | 1,420 | 1,395 | 1,390 | 1,415 | 1,415 | ||

| Total equity | 73.2 | 77.9 | 75.7 | 68.9 | 67.6 | 66.6 | 66.8 | 66.8 | ||

| Market share Price$ | 30.0 | 44.8 | 30.2 | 27.0 | 24.2 | 16.9 | 13.7 | 11.9 | ||

| Market Cap$ | 41.1 | 61.4 | 41.3 | 36.9 | 33.1 | 23.2 | 18.8 | 16.3 | ||

| Market Cap EUR | 36.6 | 54.7 | 36.8 | 32.9 | 29.4 | 20.7 | 16.7 | 14.5 | ||

| Discrspency bet. Accounting & Market-based Equity | 50% | 30% | 51% | 52% | 56% | 69% | 75% | 78% | ||

| Simple, market price derived leverage (Equity/Net Assets) | 2.53% | 3.53% | 2.52% | 2.31% | 2.11% | 1.49% | 1.18% | 1.03% | ||

| Regulatory Accounting (Fully loaded CRR/CRD4 Leverage Ratio in %1) | 3% | 3% | 4% | 4% | 3% | 3% | 3% | 3% | ||

| Leverge Multiple | 39.5x | 28.3x | 39.7x | 43.2x | 47.4x | 67.3x | 84.5x | 97.4x | ||

| Fully Loaded CRR/CRD4 Tier 1 capital2 | 50.7 | 52.5 | 51.9 | 51.5 | 48.7 | 47.3 |

|

|

||

|

|

||||||||||

| Fully loaded CRR/CRD4 Leverage Ratio in %1 | 3.5 | 3.4 | 3.6 | 3.6 | 3.5 | 3.4 | 3.4 | 3.4 | ||

| 1 Based on current CRR/CRD 4 rules (including amendments with regard to leverage ratio of Commission Delegated Regulation (EU) 2015/62 published in the Official Journal of the European Union on January 17, 2015). | ||||||||||

| 2 Regulatory capital amounts, risk weighted assets and capital ratios are based upon CRR/CRD 4 fully-loaded. | ||||||||||

Here’s What A Real, Live Veritaseum 5x Short DB Smart Contract Looks Like to Our Research Subscribers

If you haven’t heard, we’re giving out free, fully smart contracts as a 5% rebate to anyone who purchases any of our research packages above the introductory novice $50 level. This is not your Daddy’s rebate! The rebate actually gets larger as DB goes down in price. For those who may be coming late to the party, we can offer a 5x long gold (or even a long gold, short DB) smart contract rebate as well. Of course, the bulk of our research targets banks and entities other than DB, but I thought we’d make DB the subject of the rebate to drive the point home. Below is an actual contract crafted off of the price of a single share of DB for about 2 weeks.

The research and knowledge subscription module “European Bank Contagion Assessment, Forensic Analysis & Valuation” contains a full report of a very large European Deutsche Bank counterparty that faces a full 27% downside from current levels. It appears as if no one suspects a clue. It also contains much, much more (including at least 3 to 5 suspect banks). We can break this apart a la carte, if requested.

The post Even High School Kids Can See That Massive Systemic Risk That Deutsche Bank Represents appeared first on crude-oil.top.