Market dislocations occur when financial markets, operating under stressful conditions, experience large widespread asset mispricing.

Welcome to this week’s edition of “World Out Of Whack” where every Wednesday we take time out of our day to laugh, poke fun at and present to you absurdity in global financial markets in all its glorious insanity.

While we enjoy a good laugh, the truth is that the first step to protecting ourselves from losses is to protect ourselves from ignorance. Think of the “World Out Of Whack” as your double thick armour plated side impact protection system in a financial world littered with drunk drivers.

Selfishly we also know that the biggest (and often the fastest) returns come from asymmetric market moves. But, in order to identify these moves we must first identify where they live.

Occasionally we find opportunities where we can buy (or sell) assets for mere cents on the dollar – because, after all, we are capitalists.

In this week’s edition of the WOW we’re covering an update to indexing lunacy

In a previous edition of the WOW I wrote about a bubble in dumb money, and in it we looked at the massive drawdowns in capital from hedge funds in favour of “passive investing” via ETFs. Investors have a point. Why pay 2/20 when you can pay as little as 0.09% for an ETF which appears to do pretty much the same thing as a hedgie?

Two reasons that a 10-year old should be able to provide:

- If you don’t know what you’re buying, then how the heck are you going to know when to sell?

- Buying an ETF that is “low vol” creates a self fulfilling cycle. You’re buying it because of its volatility relative to other ETFs and asset classes. The more you buy it the lower the volatility measure – ergo the more you have to buy it. Genius, until the inevitable happens.

I summed my thoughts up with the following:

I fear we’re about to find out how smart “smart beta” really is. When the inevitable happens and Bob and Mabel, together with their millennial grandkids, Peach and Cloud, lose their shirts there’ll be no-one there to explain to them, “sorry, snowflake but did you realise that over half of the index you bought was sporting P/E and P/B ratios that have only existed a couple of times before?”

To help us along today in providing a granular view of how truly silly indexing really is I’m leaning on my buddy Harris Kupperman (Kuppy) who, after our discussions on the topic and some sifting through the entrails of ETFs, offered up the following:

So, this should be pretty easy to sort out.

Crawford & Co has two classes of stock, A and B. The A shares pay a dividend that is 2 cents a quarter higher than the B shares. There are differences in voting rights, but as there’s a control shareholder, those are irrelevant.

Therefore, a simple analysis says that the A shares ought to trade at a moderate premium to the B shares to account for the nearly 1% higher annual dividend yield. NOPE!! The B shares are in the Russell 2000 index and the B shares now trade at roughly a 35% premium to the A shares.

Now, I’m not here to pass judgement on the investment merits of Crawford and the A or B shares. I have done no analysis on the company and have no opinion on if it is a good investment or not. However, I know that the A shares are better than the B shares as you get a higher dividend and there is no logical reason for the B shares to trade at a huge premium except that the Russell 2000 index has to keep buying them as more money is allocated to the index.

Two years ago, I noted how index funds and ETFs were warping asset valuations and creating opportunities for those who were willing to seek them out.

This trend has only accelerated since then and has grown from something of a curiosity in certain asset classes into a true bubble that is doomed to eventually pop. There are now hordes of overvalued assets that have no justification for their overvaluation, except that index funds have to own them. Like all bubbles, this one too will burst.

In the interim, there will be huge opportunities created by how index funds misallocate capital. As I said earlier, I know nothing about Crawford, but if I wanted to own it, I sure as hell wouldn’t be buying the B shares when compared to the A shares. Additionally, I feel pretty confident in saying that at some point in my career, the A shares will trade at a premium to the B shares—as they deserve to.

At the same time, I wouldn’t be betting that this spread collapses any time soon either. Shorting indexing has been a widow-maker for many in the hedge fund industr y— it’s hard to fight against fund flows.

In finance, when a trend gets in motion and the marketers start pushing it (indexing and ETFs today) you can expect it to go further than is logically possible, but the hangover will be pretty epic. Along the way, there will be a lot of money made by better understanding the flaws in these indexes and front running them — much as I front-ran the marketing department back in March.

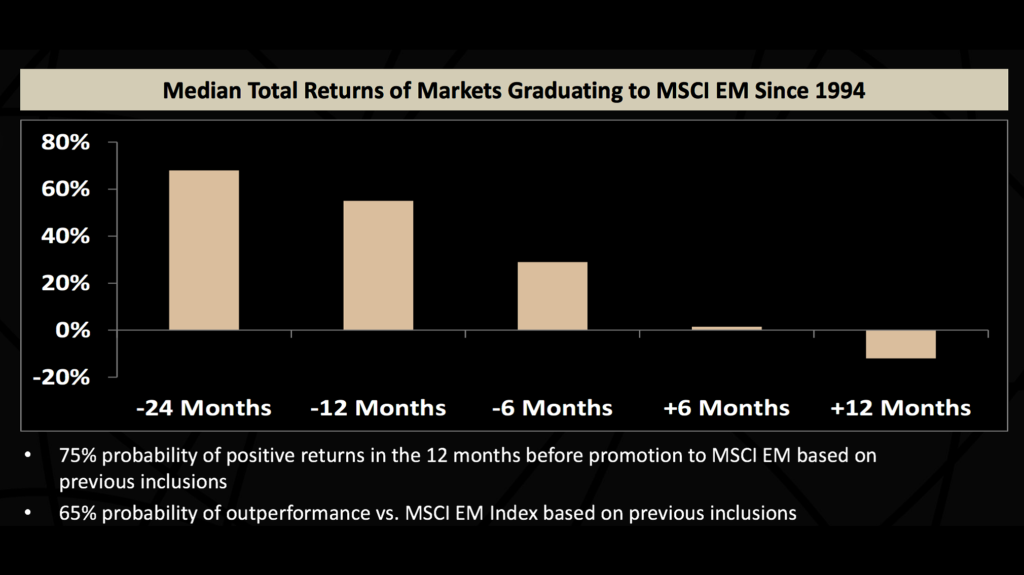

As a final note, I’d like to share a chart with you from Passport Capital showing the median total returns of markets graduating to the MSCI EM since 1994. If you can’t beat the indexers, you might as well make money off of them by getting there first.

I think it’s probably worth going back to that article from 2 years ago because it shows exactly how we made money on similar anomalies.

Think of it this way, as the indexing movement has grown, so have the assets under management — leading index funds to become key factors in access to capital. You now have really bad companies that have overstated market valuations, simply because the index has to buy it — yet you have high quality companies that should get access to capital, but are starved because they are not in the index, or not in the index at an adequate weighting.

In the real world, we call this socialism—basically starving the strong in order to prop up the stragglers. In the investment world, this is called indexing.

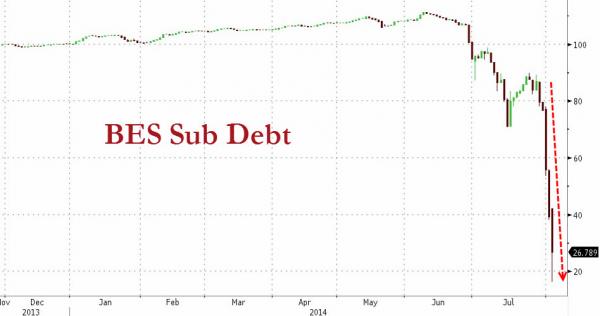

Rather than continue to bemoan modern portfolio theory, I’d rather focus on how this shift in asset allocation will create opportunities. No chart better illustrates this than the performance of Banco Espirito Santo 2023 subordinated debt:

Does anyone not know that European banks have issues (remember this was 2 years ago)? Does anyone actually believe that the European financial crisis is “solved?”

Any proper perusal of the financial statements would tell you that many European banks have “issues.”

Banco Espirito Santo didn’t suddenly have a problem — it has been troubled for a very long time. The difference is that about four weeks ago, a payment at the parent company was missed and someone suddenly noticed that the problems mattered.

Look at the chart above—the sub debt traded over par, just 5 weeks ago!! That is what happens when the financial system is managed by indexers. They simply buy what they’re told to buy—they do no research. If it is in the index, they need to own it, and we all know that bonds have been a very hot product with lots of inflows over the past few years.

How do you make money off of this? The key is research and knowledge. The good news is that all sorts of assets are mispriced. In the past, these would be mispriced because humans made mistakes in valuing them. Now they’re mispriced because they are part of a big index and some computer keeps buying them—creating a situation of overvaluation. Or they aren’t yet part of the index and no one knows they exist.

An 80% gain in a month from having realized that a debt payment at a parent company would be missed, is a huge gain. There are more gains like this out there.

Chris again…

My question for today:

Cast your vote here and also see what others think

Cast your vote here and also see what others thinkBottom line: there is no such thing as passive investing. It’s like passive sex. How it works I’ve no idea. But I just know that it doesn’t.

– Chris

“I own last year’s top performing funds. Unfortunately, I bought them this year.” — Anonymous

Liked this article? Don’t miss our future missives and podcasts, and

get access to free subscriber-only content here.

————————————–

The post Indexing Lunacy appeared first on crude-oil.top.