Encouraging rebound for stock markets

The prospect of a trade deal between the US and China is providing a major boost to the markets on the final trading day of the week.

The week got off to a shaky start following a dreadful October which very much lived up to its reputation. What’s come since is exactly what the doctor ordered though, with markets not only stabilising and avoiding further plunges but actually eating significantly in to the losses that cause so much distress.

I think investors will be feeling much more at ease now, although it’s still too early to call the end of the sell-off. The first test has been passed, there’s a good chance more will follow. Naturally though, all this talk of a trade deal between the world’s two largest economies that are currently engaging in a tariff tit-for-tat, is a supportive factor that could prevent another slump.

Trump’s China trade announcement timing very convenient

The timing of the announcement is very curious though, coming less than a week before the midterm elections. Trump has been a cheerleader of the markets since his election victory and the timing of the sell-off will have really frustrated him, even if the declines we’ve seen pale in comparison to the post-election rally.

It would seem this call comes at a very opportunistic time as it stops the rot in the markets and gives the impression that after months of tariffs and fiery rhetoric, progress is being made on improved trade terms with China. It’s a win win for Trump. I just hope the cynic in me is wrong and this is an important first step towards better trade relations between the two.

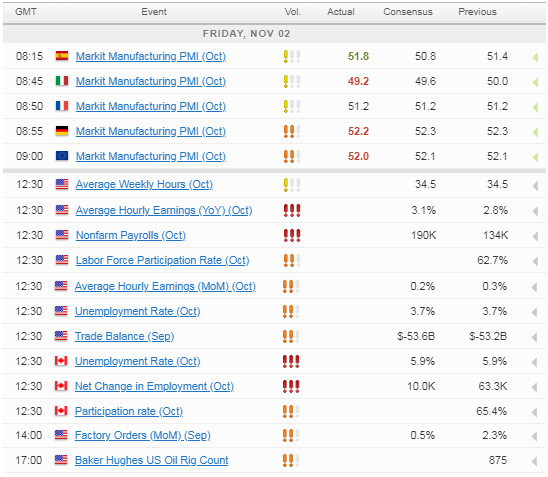

EUR/USD – Euro rally continues as German, Eurozone PMIs meet expectations

Will US jobs report be the catalyst for another sell-off?

With investors once again in a cheery mood, it seems the perfect time for a report on the health of the US labour market. The jobs report is widely regarded as the most important economic release each month and coming just before the midterms, it could be even more so than normal. The question is, would a stellar report prove to be a timely reminder of the health of the economy ahead of the election or be the next catalyst for a sell-off as investors fret about interest rates.

The unemployment rate and NFP will write the headlines but it’s the average hourly earnings that traders will be most focused on as this is more likely to directly influence interest rates. Earnings are expected to have risen by 3.1% last month, the first time they’ve exceeded 3% since 2009, in a further sign that the labour market is tight. Given what this could do to inflation and interest rate expectations, it will be interesting to see how traders respond if this number is hit, or even exceeded.

Kiwi retreats from one-month high

Return of risk appetite may not be bad news for Gold

Gold rallied strongly on Thursday on the back of weakness in the US dollar. The rally has quickly run out of steam though, as traders perch themselves back on the fence ahead of the NFP report. The return of risk appetite could be a bearish sign for Gold, given how it’s benefited from its safe haven status as of late. That said, if this is accompanied by real progress on Brexit and Italy and improved sentiment towards those currencies on the back of it, then a weaker dollar could give Gold another lift and keep it elevated.

Is the oil decline nearly over?

Oil is continuing to amble lower, taking its losses to more than 15% since peaking at the start of October. A combination of factors continues to weigh on Brent and WTI from slower global growth expectations to rising inventories. The story of only a month ago of a tight oil market driven by Iranian sanctions and a reluctant OPEC+ filling the void has been lost altogether and with it the bullish fever that got people talking about $100 a barrel. As was the case before, I think the latest move is a little overblown given how little has changed and Brent approaches $70 and WTI $62.

Economic Calendar

For a look at all of today’s economic events, check out our economic calendar.