By Chris at www.CapitalistExploits.at

A reader asked me some time back what I thought about a particular ETF. I told him I often hate ETFs and promised to provide a more detailed explanation as to why some day. Today is that day.

ETFs which simply hold equities or bonds are mostly fine.

ETFs with derivatives as their underlying collateral decay by design. Bad!

And ETFs with futures as an underlying that are leveraged will all go to zero. It’s a mathematic certainty, as reliable as knowing James Bond will always make it out alive even if along the way the villains throw a few monkey wrenches in the way.

If you are looking to invest for the long term, levered ETFs will be as successful for you as you would be trying to cut off your thumbs with a wooden spoon.

In fact, if your time horizon is long enough shorting leveraged ETFs is quite possibly the most certain investment you can probably make in this lifetime. Like Bond you’ll absolutely make it out alive and win. The script is already written in the math.

That’s the short version. If you don’t care about why stop reading now but etch the above into your mind and you’ll save yourself a lot of money and pain.

For everyone else here’s why.

Contango and Roll Decay

Contango is just a fancy name for when the spot price is lower than the future price.

Contango is also a very “normal” market, one which central bankers are incidentally doing their damndest to turn on its head but that’s a discussion for another day after a stiff drink.

In last week’s edition of the WOW I discussed the VIX. Now since the dawn of creation VIX futures have been in contango. The iPath S&P 500 VIX Short term futures ETF (VXX) tracks the VIX. I picked on it last week and so, like the bully I am, I’m going to go and pick on it again.

To understand why buying VXX as anything but a short term trade is a terrible idea, take a look at how it is structured. VXX tracks the S&P 500 VIX Short Term futures Index. Notional exposure is always 30 days out. In order to achieve this the futures contract is rolled every day.

For practical purposes what happens is that on day one the ETF will be in the nearest contract month. On day two it notionally sells a small portion in order to buy the next months contract repeating this process every trading day thus ensuring that the ETF is always notionally 30 days out.

Why this matters for anyone thinking of “investing” in this creature is because VXX is in contango.

Let me explain.

As I write this spot VIX Futures settling October 2019 are at $16.80. The November 2016 contracts are at $17.57 and spot VIX is at $15.91. So this means that if VIX stays at current levels, contango from spot to front month is 6% and 5% between October and November.

Right now volatility is low and it’s not unusual for the contango to run 20% month to month when volatility is high. When you annualize these figures it amounts to one heck of a headwind.

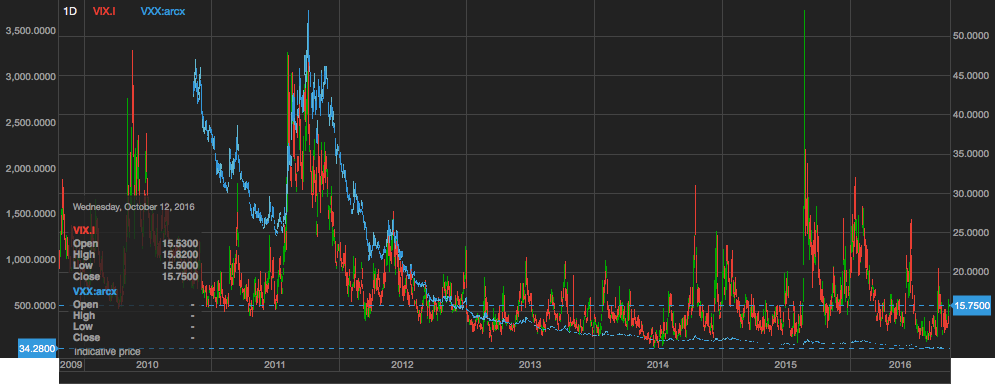

Fighting contango

This is where contango matters. The chart below shows the VIX in red and green and the VXX ETF which tracks it. You can see over time that the VXX doesn’t do what you want it to do. This is because the juice is being sucked out of it on a daily basis as contracts are rolled and the fact that the market is in contango.

Now take a look at the chart below. We’re looking at the VIX index in blue and the Proshares Ultra VIX ETF (UVXY) (levered 2x) in red and green.

Remember when volatility spiked in August of 2015?

We can see this on the chart with the VIX rising from the ashes but for those poor suckers holding UVXY which “offers 2x leverage to the VIX” you needed to have bought it just ahead of the spike and sold it immediately after in which case you’d have enjoyed roughly 2x leverage to VIX.

Anything longer and it’d have been like getting married to a pig because it was going to just keep dragging you back into the mud. Which brings me to…

Volatility: The Real Killer

Let’s take a theoretical 3 x leveraged ETF as an example. Any will do.

We’ll run the numbers on holding one of these for just two weeks. We’ll start day 1 with a value of the leveraged ETF as well as the underlying index at 100 for easy math.

| Day | Index Move | Index | 3x ETF |

| 1 | -2% | 98.00 | 94.00 |

| 2 | -3% | 95.10 | 85.50 |

| 3 | 4% | 98.90 | 95.80 |

| 4 | 5% | 103.80 | 110.20 |

| 5 | -3% | 100.70 | 100.30 |

| 6 | -1% | 97.70 | 97.30 |

| 7 | 1% | 100.70 | 100.20 |

| 8 | -3% | 97.70 | 91.20 |

| 9 | 4% | 101.60 | 102.10 |

| 10 | -1.5% | 100.00 | 97.50 |

As you can see in half the time it takes you to receive your broker statement to realise what an idiot you are, you’re down 2.5% while the underlying index hasn’t budged from where it started.

In the chart below we’ve looking at the S&P 500 index in red and UPRO which is a 3x leveraged ETF on the S&P 500 index.

S&P 500 Index (red) and UPRO 3X S&P 500 (blue)

You can see that it’s barely managed to keep up with the index over time let alone triple it, even though it sports 300% leverage. One reader wrote to me a couple years ago telling me that he’d been holding UPRO in his portfolio for over 2 years. I had to tell him he’d just bought leveraged time decay. Terrible.

The thing is he’d not even noticed as he’d been looking at the stock quote on UPRO and it seemed consistent.

Why?

Well, this is the other thing which we’ve not covered yet…

Stock Splits

Due to all the reasons just mentioned you can see why the value of these ETFs falls. As a result they are frequently reverse split. This simply makes them look more attractive to retail investors.

So for example, you can be holding 10,000 shares of a leveraged ETF in month one and a few months later you’re suddenly holding just 5,000 shares. The price may have not moved much and if you’ve been looking at the price ticker on your feed and not reconciling your broker statements you’re not going to know.

I’ve often seen financial websites which track ETFs fail to keep up with all these reverse splits, especially on the leveraged ETFs.

The job of tracking all of them and how often they’re reverse splitting must be harder than keeping up with Americas political scandals.

Lesson

So there you have it. Trade ’em, just don’t invest in ’em.

Don’t say I didn’t warn you.

Next Week

ETFs are largely designed to allow for passive investing. I want to write about the unintended consequences to passive investing because the opportunities created, by what looks awfully like a bubble in passive investing to me should not be ignored.

Until then, keep safe.

– Chris

PS: Passive investing is an oxymoron. If it’s not active, it’s speculative. Ben Graham makes this point clear:

“An investment operation is one which, upon thorough analysis, promises safety of principal and an adequate return. Operations not meeting these requirements are speculative.” — Benjamin Graham

————————————–

Liked this post? Don’t miss our future articles and podcasts, and

get access to free subscriber-only content here.

————————————–

The post Never Invest In These HORRIBLE Things. Ever! appeared first on crude-oil.top.