Submitted by Charles Hugh-Smith of OfTwoMinds blog,

This decline is inevitable in fast-expanding economies that depended on export growth and investment booms.

The fundamental context of China's economy is that it has traced out an S-Curve – as did previous fast-developing nations such as Japan and South Korea.

Gordon Long and I discuss why there's no easy fix to the S-Curve in our new video discussion Bull in the China Shop (35:25).

The S-Curve can be likened to a rocket's trajectory: first, there's an ignition phase, as the fuel of financialization, cheap labor and untapped productive capacity is ignited.

The boost phase lasts as long as credit-fueled production and consumption expand rapidly.

In the boost phase, investors and financial authorities can do no wrong. The high growth rate of credit and production overwhelms all other factors, as the virtuous cycle of expanding profits and production increases wages which then support further expansion of credit and consumption which then supports more production, and so on.

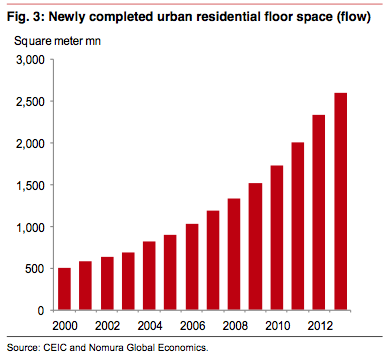

A vast tide of foreign investment fuels an equally vast expansion of fixed capital assets such as factories and new homes. (The chart below depicts the astronomical amounts of new square footage constructed in China every year.)

But then the fuel of financialization is consumed, and the previously fast-growing economy slows to stall speed. Depending on how much leverage, corruption and wealth has piled up in the boost phase, this phase may last a few years. This is the top of the S-Curve.

As the economy weakens, everything that worked in the boost phase no longer works: expanding credit no longer boosts growth, inflating yet another real estate bubble no longer generates a widespread wealth effect, and every effort to shift from being an export-dependent economy to a self-supporting consumer economy fails to achieve liftoff.

This decline is inevitable in fast-expanding economies that depended on export growth and domestic investment booms fueled by exploding credit and leverage. In the decline phase of the S-curve, doing more of what succeeded spectacularly now fails spectacularly.

Building more ghost cities and investment flats doesn't fix what's broken:

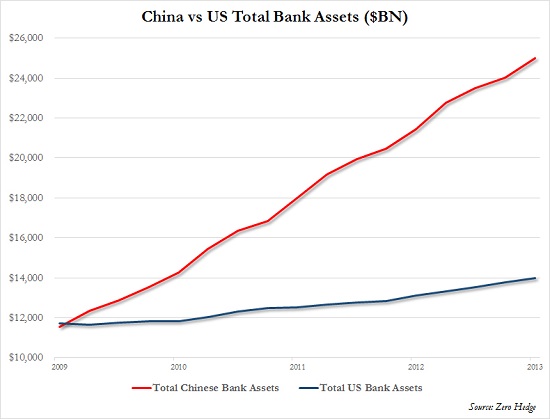

Expanding credit and the banking sector doesn't fix what's broken:

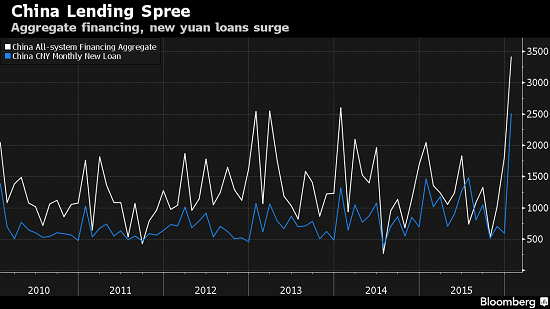

Loaning more money to bankrupt entities doesn't fix what's broken:

And while authorities struggle to restart growth with tools that no longer work, China is burdened by immense costs that have yet to be paid: the external costs of rampant pollution include not just cleaning up the sources of pollution but treating the illnesses created by that pollution.

The clean-up is a non-trivial task that will eventually cost trilions of yuan–money that will no longer be available to prop up failing enterprises and local governments.

Pity poor China: there's no easy fix to the S-curve. Everything that worked so well for 30 years is only making the economy more precarious. Gordon Long and I explain why all this matters to the U.S. economy and the global economy in Bull in the China Shop (35:25).

The post Pity Poor China: There’s No Easy Fix To The S-Curve appeared first on crude-oil.top.