US equity markets are expected to open a little lower on Wednesday, tracking similar marginal losses in Europe as traders look ahead to the third Presidential debate, appearances from Fed policy makers, earnings and oil inventory data.

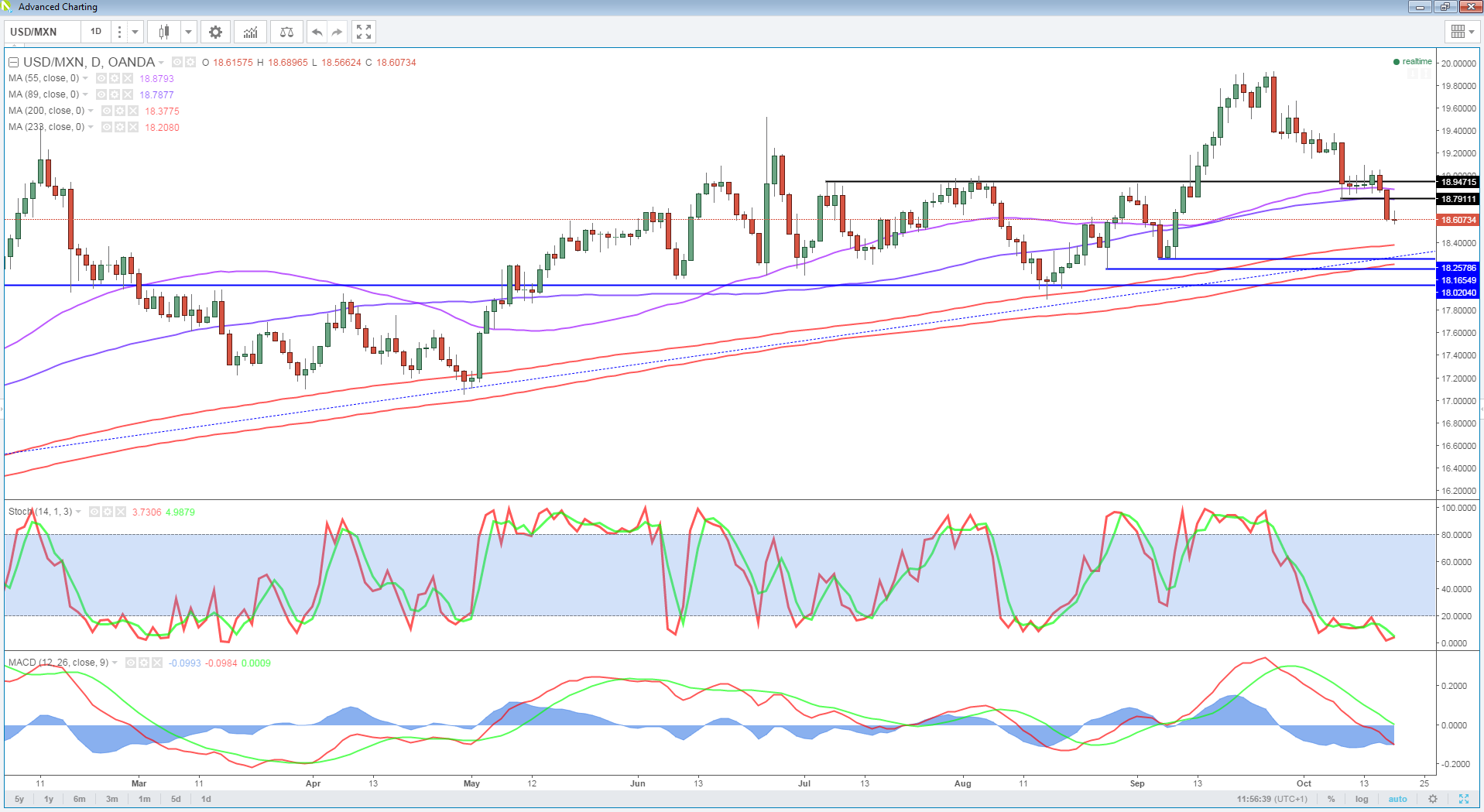

Markets have been very responsive to how the election campaign has gone so far, particularly those most vulnerable to the outcome such as Mexico, with the Peso experiencing large amounts of volatility. Hillary Clinton storming ahead in the polls following a series of damaging reports about Donald Trump has given a big boost to the Peso, which now trades at its highest level since 8 September. Should Trump once again fail to secure a victory in tonight’s debate, it could aid risk appetite heading into tomorrow’s session and provide another boost for the Peso.

OANDA fxTrade Advanced Charting

USD/CAD – Canadian Dollar Edges Higher Ahead of BoC Rate Statement

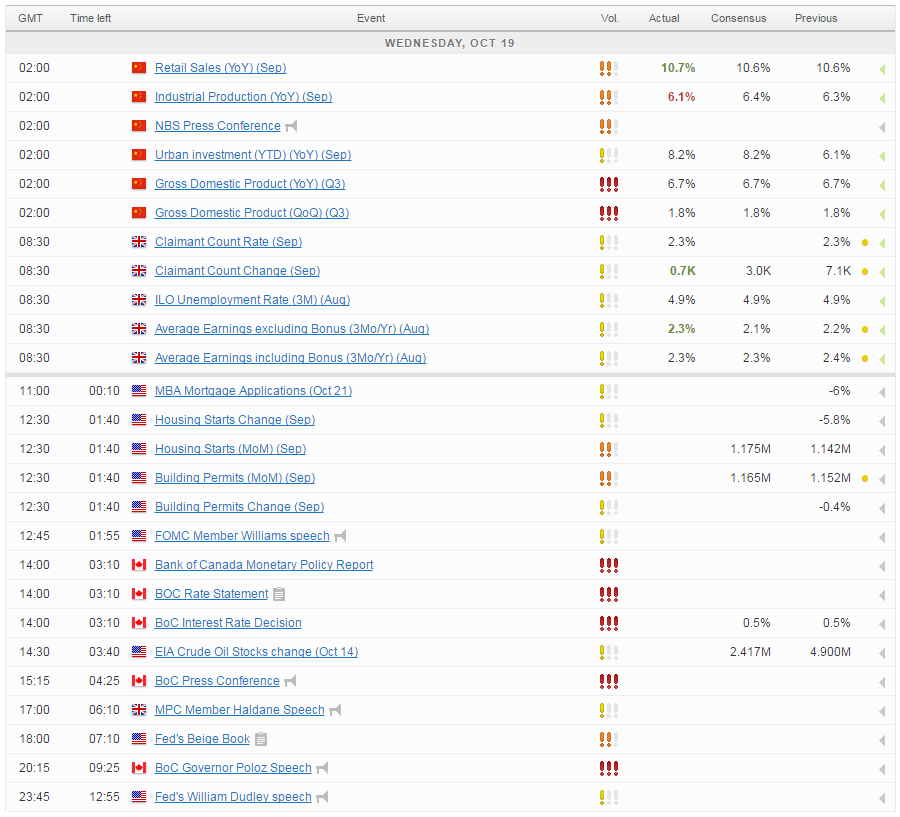

Rate hike expectations for December have been pared in recent days after rising above the 70% threshold that many see as being necessary before the Fed will approve. While I don’t think this necessarily reflects a significant change in market expectations ahead of the meeting, it does show that more is needed to convince investors that the Fed will raise rates this year. While we won’t get any notable economic data today, we will hear from three Fed officials – William Dudley, Robert Kaplan and John Williams – and get the latest Fed insight on the economy with the release of the Beige Book. Dudley appears to be coming round to the idea of a hike – which would see him join the three dissenters from the last meeting – having recently claimed that he expects one this year. Kaplan is a voting member on the FOMC next year and so his comments will also be very valuable.

Corporate earnings season will remain in focus today, as 25 S&P 500 companies report on the third quarter. With the Fed keen on raising interest rates, it’s important for companies to fill the void left by ultra-loose monetary policy, something they have struggled to do this year having found themselves in an earnings recession. With indices looking a little toppy and susceptible to significant downside, earnings season could be a key sentiment driver in the coming weeks.

The one piece of data that people will be keen on today is the EIA crude oil inventories, with oil prices trading around their highest levels since June and struggling to break higher. A build of 4.9 million barrels last Thursday broke a five week streak of inventory drawdowns which had helped lift oil prices above $50 a barrel. While a second increase of 2.4 million barrels is expected today, API reported on Tuesday that stocks had actually fallen again by 3.8 million barrels which suggests we could be in for a surprise and further upside in Brent and WTI.

For a look at all of today’s economic events, check out our economic calendar.