Submitted by David Stockman via Contra Corner blog,

The casino is incorrigible. After a monumental short squeeze that has lifted the averages right into the jaws of danger, Goldman Sachs has the temerity to print the following:

“Our model suggests SPX calls are more attractive than at any time over the past 20 years”.

There must have been a mullets’ breeding frenzy awhile back because it’s hard to fathom how Goldman has any real customers left. Then again, its current preposterous call is just indicative of the horrible threat heading menacingly toward what remains of main street’s 401k investments.

To wit, the Fed and other central banks have thoroughly falsified financial market prices and destroyed all of the ordinary mechanisms of financial discipline. Foremost among these are short sellers and a meaningfully positive cost of carry trades.

Markets are therefore unhinged from any connection to fundamental economic and financial reality, meaning that they are capable of an extended period of spasmodic deadcat bounces that will have only one end result.

Namely, the naïve and desperate among main street investors who still, unaccountably, frequent the casino will presently be taken out back and shot yet another time. The market technicians are pleased to call this “distribution”. Would that someone on Wall Street man-up and amend the phrase to read ” distribution…….of losses to the mullets” and be done with the charade.

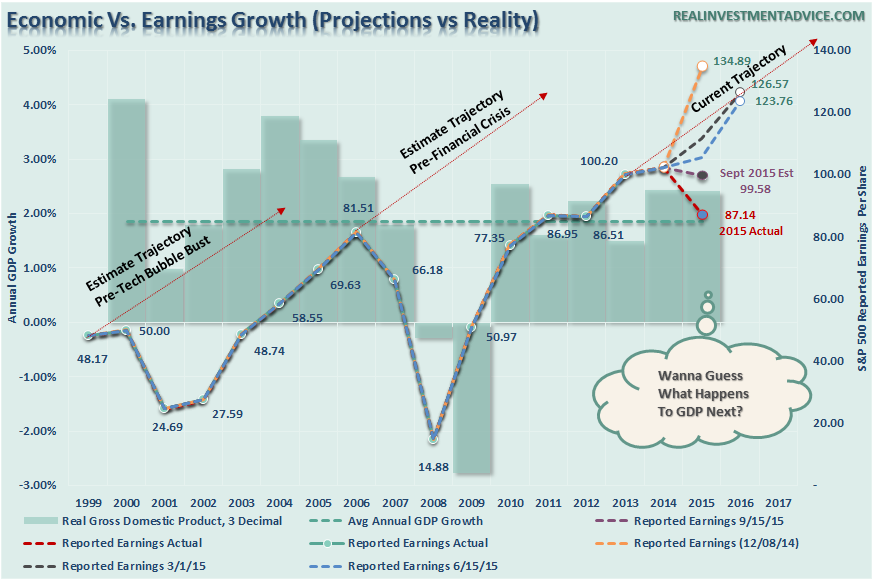

The S&P 500 is heading through 1300 from above long before it ever again penetrates from below its old May 2015 high of 2130. And now that 97% of Q4 results are in, there is a single number that proves the case.

Reported LTM profits as of year-end 2015 stood at just $86.46 per S&P 500 share. That particular number is a flat-out bull killer. At a plausible PE multiple of 15X, it does indeed imply 1300 on the S&P 500 index.

It also represents an 18% decline from peak S&P 500 reported earnings of $106 per share back in September 2014. And more importantly, it means that the robo-machines and hedge fund gamblers have traded the market back up to 23.1X earnings.

That’s off the charts…….except for when recession has already arrived unannounced by the hockey stick factories of Wall Street.

But here’s the thing with respect to the scarlet 23.1X numerals now painted on the casino’s front entrance. It comes at a time when the so-called historical average PE ratios are way too high for present realities. That is, in a world sliding into a prolonged deflationary decline, capitalization rates should be falling into the sub-basement of history.

Why? Because current earnings are worth far less than normal owing to the prospect that renewed earnings growth anytime soon is lodged somewhere between zero and none.

So when capitalization rates should be plunging the casino has them soaring, while pretending its all awesome on the earnings front. In a nearby post, Lance Roberts puts the story in devastating historical context.

For the third time this century, corporate earnings are already in free fall, yet the Wall Street hockey sticks are still pointing archly to the upper right of the chart.

Yet this time the backstory is even sketchier. When reported S&P 500 earnings peaked at $84.92 per share in June 2007 (LTM basis), they had grown at a 6.8% annualized rate since the prior peak of about $54/share in Q3 2000. By contrast, at the reported $86.46 level for the LTM period ending in Q4 2015, the implied 8-year growth rate is…….well, nothing at all unless you prefer two digit precision. In that case, the CAGR is 0.22%.

That’s right. Based on the kind of real corporate earnings that CEOs and CFOs must certify on penalty of jail time, profits are now barely above the June 2007 level, and are once again heading down the slippery slope traced twice already during this era of central bank bubble finance.

Yes, the sell side stock peddlers will tell you that notwithstanding the fact that Uncle Sam spends upwards of $1 billion per year pursuing accounting malefactors, these GAAP profits are to be ignored because they are chock-a-block with non-recurring items.

Well, yes they are. As an excellent recent Wall Street Journal investigation showed, the Wall Street version of ex-items earnings came in for 2015 at $1.040 trillion for the S&P 500. But that was 32% higher than actual GAAP earnings of $787 billion!

.

Not exactly. The above chart has been generated over and over and has been spectacularly wrong nearly as often, and most especially at turning points in the business cycle.

Indeed, the yawning $253 billion gap between reported earnings and the Wall Street ex-items concoction for 2015 is nearly the same magnitude as the disconnect in 2008/early 2009. And like back then, the massive one-timers consisted of real corporate cash and capital that was destroyed——more often than not owing to bad business decisions that had earlier resulted from central bank falsification of interest rates and the price of debt and equity securities.

For instance, during 2015 one part of the gap was accounted for by the fact that the energy sector of the S&P 500 reported actual losses of $45 billion collectively but on an ex-items basis claimed profits of $48 billion. Did that $93 billion difference amount to a financial nothing?

No it didn’t. Instead, it was comprised primarily of massive write-downs of the carrying value of oil and gas reserves. Yet it was the global credit boom enabled by central banks which first drove the price of oil above $100 per barrel and encouraged massive malinvestment in high cost and excessive reserves.

And then, to add insult to injury, it was the drastic post-crisis repression of interest rates under the ZIRP and NIRP regimes which ignited a massive scramble for yield among money managers and homegamers alike. This central bank caused deformation, in turn, encouraged E&P companies to borrow upwards of $400 billion on the junk bond and junk loan market to fund investments in shale and elsewhere which were never remotely economic.

Those giant write-downs may be construed by Wall Street as non-recurring irrelevances, but in fact they amount to dead weight losses of real capital.

The same is true with the other sectors analyzed by the WSJ investigation. Materials companies reported $13 billion in GAAP earnings compared with $30 billion in ex-items profits. And health-care companies earned $104 billion under GAAP versus $157 billion as imagined by Wall Street analysts. Yet once gain, the $70 billion difference in these two sectors wasn’t chump change, nor was it invisible fairy dust.

For the most part it represented asset write-offs and restructuring charges from uneconomic investments and failed M&A deals. That is, the very thing which central bank falsification of financial prices inevitably fosters.

Even in tech, the degree of earnings fudging by Wall Street last year was egregious. While the hockey stick brigade dutifully reported $218 billion of aggregate profits for the tech sector, the reports sent to the SEC showed only $176 billion. Among that $42 billion of invisible red ink was a lot of busted M&A deal write-offs and stock options costs that do absolutely dilute shareholder earnings.

In a recent BloombergView post on the folly of negative interest rates Michael Schuman got it spot on. While he was focusing on the absurdity of the fact that investors are now paying cash to the government of Japan when it borrows ten year money, the general principle is universal.

The culprit is the Bank of Japan. The entire purpose of its unorthodox stimulus programs — quantitative easing, negative interest rates — is, in effect, to get prices wrong: to press down interest rates below where they would normally go and force banks to lend money in ways they normally wouldn’t. The BOJ, in other words, is trying to alter prices to change the incentive structure in the economy in order to engineer certain results — to increase inflation, encourage investment and spark growth.The problem is that the BOJ hasn’t achieved any of those objectives. Inflation in January, by one commonly used measure, was a pathetic zero. Gross domestic product has contracted in two of the past three quarters.

Instead, the BOJ is creating new problems by undermining the price mechanism. The central bank is buying up so many government bonds that it has effectively stripped them of risk to the investor and cost to the borrower. Investors probably bought up the bonds with negative yields speculating that they could flip them to the BOJ.

That’s what might otherwise be called an ambush. The trillions of speculator dollars crowded into trades of this type throughout the global financial markets will never get through the narrow door of liquidity that remains in the casinos. The dotcom and the post-Lehman meltdowns were only the rehearsal.

![]()

Запись The Price Isn’t Right – How Central Banks Are Fixing To Ambush The Casino впервые появилась crude-oil.top.