It was always expected to be a volatile week for financial markets given the number of major central bank announcements, US jobs report release and the constant flow of earnings reports, but the resurgence of Donald Trump in the polls so close to election day has seriously rattled investors.

Since the FBI reopened its case into Hillary Clinton’s emails last Friday, her substantial lead in the polls has been decimated and some now even show Trump in the lead. It’s been clear for some time now that markets would much prefer the stability that a Clinton victory would bring for the US economy and the reaction over the last 24 hours or so since the polls started to change so dramatically just confirms this. Trump risk is well and truly being priced in again.

Mexican Peso’s Bout Of “Trumpitis” Continues…

The sell-off in equity markets is not being helped by sharp declines in crude prices in recent days.

OANDA fxTrade Advanced Charting Platform

As cracks in the OPEC production agreement have started to appear, it has become clear that markets bought into this way too early and now they’re starting to correct themselves. The sell-off over the last 24 hours has also been helped by a large inventory build reported by API on Tuesday, which may be confirmed by EIA later today.

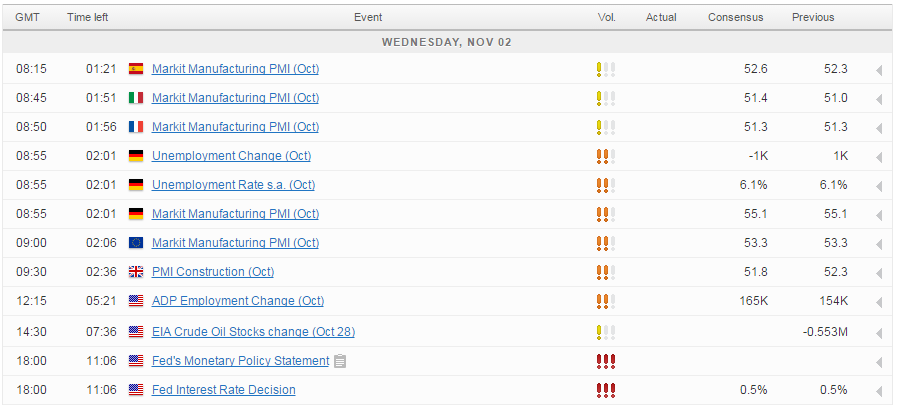

Throughout the morning we’ll get manufacturing PMI data from throughout the euro area and the UK but this will likely be somewhat overshadowed by what’s going on in the US. Not only will the election remain front and centre today but we also have the small issue of the Federal Reserve rate decision and statement, which up until last Friday was likely to be the main event this week.

Asian Markets Rocked by Election Uncertainty

While a rate hike this evening is extremely unlikely, particularly given the drama around the election in recent days, December still remains very much on the cards, although it will be very interesting to see whether this remains the case if Trump emerges victorious next week. There will be no press conference alongside the decision today which will put all the emphasis on the accompanying statement and whether the Fed decides to drop a strong hint that they’re almost in agreement that they’ll mark the anniversary of the first hike in almost a decade with a second.

For a look at all of today’s economic events, check out our economic calendar.