Submitted by Lance Roberts via RealInvestentAdvice.com,

There was little doubt going into the election who was going to win. Whether it was the mainstream media, the polls, or the political punditry; the answer was clear.

“Hillary was going to be the 45th President of the United States.”

But it did not turn out that way.

As I discussed many times on my Houston morning drive show, “The Lance Roberts Show,” what the “experts” missed was evidence of another “Brexit.”

As with the “Brexit,” the polls, Wall Street, and the experts were wrong as the “Shy-Tory” effect took hold. This effect was derived from individuals being unwilling to express their opinions in fear of persecution from the counter party, but voted their beliefs at the polls. While the market “bet” Britain would stay in the E.U., the vote turned out differently.

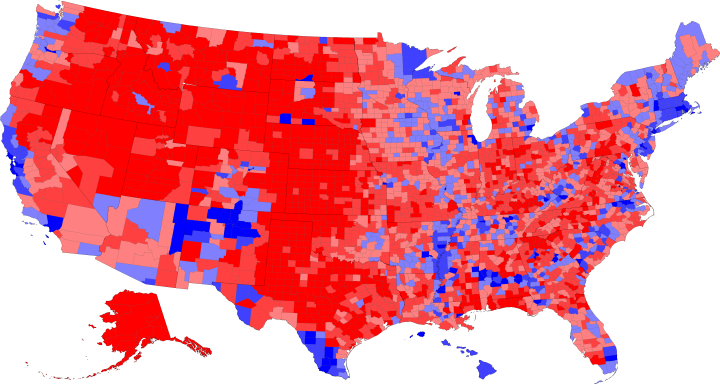

The same was clearly evident during the election campaigns in the U.S. as polls clearly indicated a favorability towards Clinton, but massive crowds were gathering a Trump rallies. The were clear indications the “Shy-Trump” phenomenon was present as individuals who wanted “hope and change” remained quiet during the campaigns, but voted loudly when it counted. This is shown in the graphic below of the county voting outcomes.

The vote was really not as much about “Clinton vs. Trump” as it was a referendum on the last 8-years of economic weakness, lack of wage growth and a constant attack on America’s “way of life.” The vote was about wanting what Obama promised but failed to deliver – “hope and change.”

My partner Michael Lebowitz just penned an excellent article on this point stating:

“There is ample evidence that despite the narratives of the Federal Reserve, media pundits, and most policy wonks, the economy is failing most Americans. While there are many ways to show the deterioration of the U.S. economy and the consequences endured by its citizens, we selected charts we deem to be the most telling.

We hope that no matter who you voted for, you study these graphs to better understand the impetus behind Trump’s victory. More importantly, we hope this helps everyone better grasp why economic policy must change before the consequences become dire.”

Importantly, when it comes to investing or economic policies, “timing is everything.” While there is currently high expectations for the future of economic policy, there is a strong headwind that must be fought. Unlike when President Obama took office, immediately following the financial crisis when unemployment was high, economic growth was decimated and “fear” ruled investors; Trump enters office with everything reversed. Policies that boosted economic growth in 2009-2011 will not be nearly as effective today. Infrastructure spending won’t have the same impact as what was seen in 2009. Higher rates and inflation will slow economic growth as it impacts an already strapped consumer. Debts and deficits will rise further slowing the economy as well.

The point is that while there is much hope Trump’s economic plan will facilitate stronger growth, and it ultimately will, it will not forestall the onset of an economic recession and a negative shock to stocks within the next 12-18 months.

The economic expansion over the last 8-years is already extremely long by historical standards and retailers, consumers and businesses are already showing signs of wear. Furthermore, the rise in both LIBOR and Treasury rates are already increasing borrowing costs for both consumers and businesses, further reducing future demand as people buy “payments” rather than products.

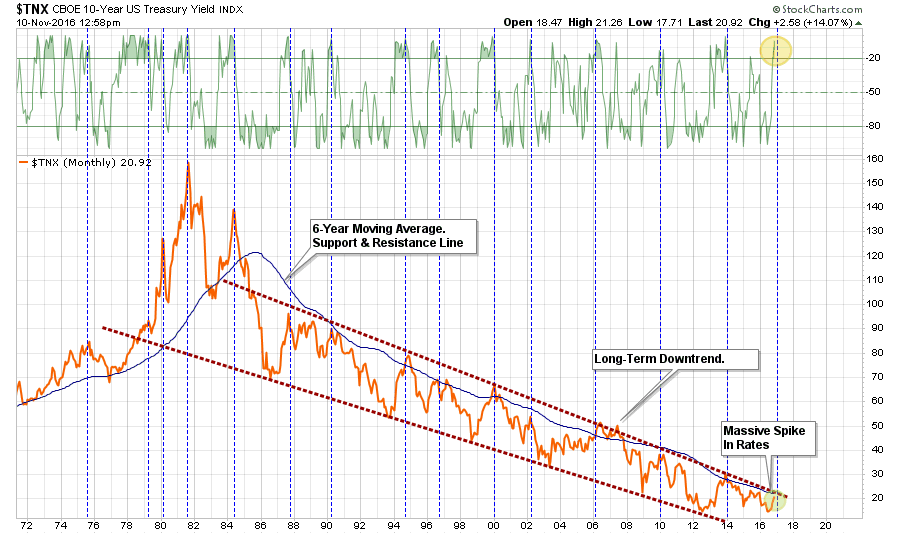

While the spike in interest rates since the election has seemed to exceedingly large, sending bond investors fleeing for cover, let’s put the recent rise back into perspective.

- Rates are now back to where they were at the beginning of 2016.

- The run down in rates was due to overblown fears of the “Brexit.”

- Rates are now normalizing back to levels of current GDP and Inflation levels which is where “fair value” remains.

- Bonds are EXTREMELY oversold making bonds an interesting asset class as compared to overbought equities.

- Rates are the top of a long-term downtrend and pushing into the 7-year moving average resistance line. The long-term downtrend is correlated to the long-term downtrend in economic growth and inflation as well. Those issues are changing anytime soon.

With the election now behind us, we can once again turn our focus back to the real drivers of financial markets over time; earnings, profits, valuations, and economic growth. There is little change in those specific dynamics to justify further increased valuations and additional speculative risk taking at this time.

Yes, you just experienced a “Trexit.” The question is now what happens next?

In the meantime, here is what I am reading this weekend.

Fed / Election / Economy

- Exiting Our Winter Of Discontent by Danielle DiMartino-Booth via Money Strong

- Apparently, If You Voted For Trump, You’re A Racist by Jim Tankersley via WashPo

- Nothing Has Changed Yet by Joe Calhoun via Alhambra Partners

- What If Trump Keeps His Promises by Tory Newmyer via Fortune

- Clinton Lost The Economic Argument by Helaine Olen via Slate

- Who Lost? by Charles Hugh Smith via Of Two Minds

- Trump Can Quickly Put Stamp On Fed by Greg Robb via MarketWatch

- Good Chance Trumped Handed A Recession by Chris Isidore via CNN Money

- Trump Economic Consequences Could Be Bad by The Economist

- Fake Capitalism by Nicole Gelinas via City Journal

- Time To Abandon GDP by Buttonwood via The Economist

- Are Better Off Today Than 8 Years Ago? by Tami Luhby via CNN Money

- Fed Reserve: All Out Of Targets by Jeffrey Snider via Alhambra Partners

- Has Job Growth Peaked by Robert Johnson via MorningStarr

- Does The Economy Need To Keep Growing? by Alana Semuels via The Atlantic

- Wall Street Has It Wrong On Trump by Charlie Gasparino via New York Post

Markets

- Stock Guru’s No Better Than Pollsters by Rebecca Spalding via Bloomberg

- Just How Big Is A Big Gross Margin by Eric Bush via GaveKal

- If This Is A Market Bubble, Election Won’t Matter by Antoine Gara via Forbes

- 5 Bullish Facts About The Market by Mark DeCambre via MarketWatch

- Election Marks Beginning Of Volatility by Jared Dillian via Yahoo

- The Views Of Yale’s Investment Guru by Geraldine Fabrikant via NYT

- How To Play The Trump Rotation by Michael Kahn via Barron’s

- A Huge Concern For Stocks by Bob Bryan via Business Insider

- Druckenmiller: I Sold All My Gold On Election Night by Tyler Durden via ZeroHedge

Interesting Reads

- Taxpayers Are Still Bailing Out Wall Street by Renae Merle via Washington Post

- Want To Fix Infrastructure? Get Government Out by Lawrence McQuillan via IBD

- The U.S.’s Misplaced Admiration For Europe by Noah Smith via Bloomberg

- 5-Signs It’s Time To Change Your Advisor by Martin Pelletier via Financial Post

- China’s Gift To Trump: Crisis by Tom Orlik via Bloomberg

- AI Is Here: Now What? by Thomas Hemphill via Nat. Center For Policy Analysis

- If You Build It (Infrastructure), They Won’t Come by Stephen Entin via IBD

- Should Retirement Age Be 76 by Chris Farrell via MarketWatch

- US Company Creation Crashes Most On Record by Tyler Durden via ZeroHedge

- Recessions, Predictions & The Stock Market by Pater Tenebrarum via Acting-Man blog

- High Risk & Low Conviction by John Hussman via Hussman Funds

- The Last Time This Happened It Wasn’t Good by Dana Lyons via Tumblr

- You’re Crazy by Jesse Felder via The Felder Report

“If the question is when markets will recovery, a first-pass answer is never.” — Paul “Habitually Wrong” Krugman

The post Weekend Reading: Markets Experience A “Trexit” appeared first on crude-oil.top.