Submitted by David Stockman via Contra Corner blog,

The desperate suzerains of the Red Ponzi are incorrigible. There appears to be no insult to economic rationality that they will not attempt in order to perpetuate their power, privileges and rule.

So now comes the most preposterous gambit yet. Namely, a veritable tsunami of state handouts to foster, yes, capitalist entrepreneurs!

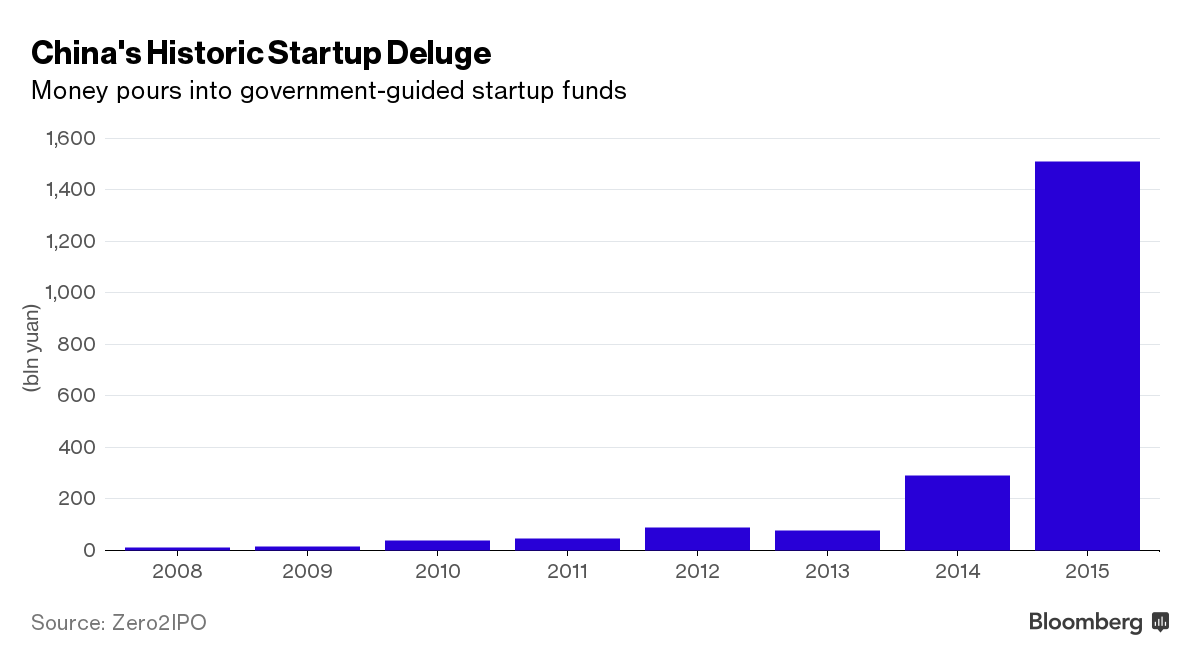

That’s right. As described by Bloomberg, Premier Li Keqiang gave the word, and, presto, nearly $340 billion poured into an instantly confected army of purported venture capital funds run by local government officialdom all over the land.

China is getting into the venture capital business in a big way. A really, really big way.

The country’s government-backed venture funds raised about 1.5 trillion yuan ($231 billion) in 2015, tripling the amount under management in a single year to 2.2 trillion yuan ($340 billion), according to data compiled by the consultancy Zero2IPO Group. That’s the biggest pot of money for startups in the world and almost five times the sum raised by other venture firms last year globally, according to London-based consultancy Preqin Ltd.

Really? These are the same folks who built themselves a 1.2 billion ton steel industry in less than two decades, representing double what they can actually use and far more capacity than the rest of the world combined. That freakish industrial eruption is now tumbling into a red hole of losses, decay, abandonment and waste, but never mind. Now the Beijing comrades are going to seed venture capitalists at 5X the rate of the entire planet?

It puts you in mind of Mao’s Great Leap Forward, which endeavored to put a steel furnace in every Chinese farmer’s back yard. Of course, when they melted down their plows and hoes for scrap, the resulting leap was not exactly forward.

The only difference is that today’s Chinese leaders wear business suits, speak the lingo of western finance and dye their hair black. Yet the very idea that Beijing could wave a wand and launch 1,600 high-tech incubators for start-ups within a few months time and mobilize 2.2 trillion yuan ($340 billion) of venture capital is a measure of the incendiary lunacy which has gripped the Red Ponzi:

The money’s in what are known as government guidance funds, where local and central agencies play some role. With 780 such funds nationwide and a lot of experimentation, there’s no set model for how they’re managed or funded. The bulk of their capital comes from tax revenue or state-backed loans.

The money is part of Premier Li Keqiang’s effort to bolster the slowing Chinese economy through innovation and reducing its dependence on heavy industry. The country began a campaign to support entrepreneurship in 2014 and has since opened 1,600 high-tech incubators for startups.

Somehow Bloomberg did manage to find one sane commentator on this colossal farce who minced no words. Gary Rieschel, founder of Qiming Venture Partners, suggested that this huge influx of cash raises the possibility of a boom-and-bust cycle like the government-led investment in China’s solar and wind power sectors, among others:

…..“They have a fantasy that if they give everyone money they’ll create entrepreneurs,” he said. But inexperienced or corrupt managers are likely to invest in dozens of regional copycats unable to get big enough to be profitable, he said. “What it will result in is catastrophic losses for the government.”

The point is, an unhinged central bank printing press and a limitless spigot of state funds will eventually create waste, not wealth. Indeed, the stated rationale for this latest burst of madness is the proof of the pudding. They are trying to shove risk capital were private venture investors won’t go——which is to say, in exactly the wrong places.

The cash is meant to “overcome the failure of pure market-oriented allocation of venture capital,” by steering investment into seed and early stages, according to Zero2IPO. The government wants to attract money to riskier startups shunned by private investors who chase quicker and surer returns in late-stage bets, Wu Qing, a researcher for the State Council Development and Research Center, told the China Youth Daily.

Indeed, the evidence that the Red Ponzi has entered a final delirious blow-off stage accumulates by the day. This Bloomberg story noted that private equity is also exploding in China. At present the are apparently 15,900 limited partnerships with nearly $1.0 trillion under management. The speculative excesses being fostered must be truly mind-boggling.

But don’t tell the gamblers still left in the Wall Street casino. They persist in the preposterous delusion that China is a $10 trillion growth miracle with transition challenges that will be deftly taken to the next level of consumption and services-based growth by the deft managers in Beijing.

No it won’t. China is an economic doomsday machine heading for a crash landing, and this latest venture capitalist gambit is just further proof.

The truth is, there is no real capitalism in China at all; it is a quasi-totalitarian nation gone mad digging, building, borrowing, spending and speculating in a magnitude that has no historical parallel.

So doing, It has fashioned itself into an incendiary volcano of unpayable debt and wasteful, crazy-ass overinvestment in everything. It cannot be slowed, stabilized or transitioned by edicts and new plans from the comrades in Beijing. It is the greatest economic trainwreck in human history barreling toward a bridgeless chasm.

And that proposition makes all the difference in the world. If China goes down hard the global economy cannot avoid a thundering financial and macroeconomic dislocation. And not just because China accounts for 17% of the world’s $80 trillion of GDP or that it has been the planet’s growth engine most of this century.

In fact, China is the rotten epicenter of the world’s two decade long plunge into an immense central bank fostered monetary fraud and credit explosion that has deformed and destabilized the very warp and woof of the global economy.

But in China the financial madness has gone to a unfathomable extreme because in the early 1990s a desperate oligarchy of despots who ruled with machine guns discovered a better means to stay in power. That is, the printing press in the basement of the PBOC—-and just in the nick of time (for them).

Print they did. Buying in dollars, euros and other currencies hand-over-fist in order to peg their own money and lubricate Mr. Deng’s export factories, the PBOC expanded its balance sheet from $40 billion to $4 trillion during the course of a mere two decades. There is nothing like that in the history of central banking—–nor even in economists’ most febrile imagings about its possibilities.

The PBOC’s red hot printing press, in turn, emitted high-powered credit fuel. In the mid-1990s China had about $500 billion of public and private credit outstanding—hardly 1.0X its rickety GDP. Today that number is $30 trillion or even more.

Yet nothing in this economic world, or the next, can grow at 60X in only 20 years and live to tell about it. Most especially, not in a system built on a tissue of top-down edicts, illusions, lies and impossibilities, and which sports not even a semblance of financial discipline, political accountability or free public speech.

To wit, China is a witches brew of Keynes and Lenin. It’s the financial tempest which will slam the world’s great bloated edifice of central bank fostered faux prosperity.

So the right approach to the horrible danger at hand is not to dissect the pronouncements of Beijing in the manner of the old kremlinologists. The occupants of the latter were destined to fail in the long run, but they at least knew what they were doing tactically in the here and now; it was worth the time to parse their word clouds and seating arrangements at state parades.

By contrast, and not to mix a metaphor, the Red Suzerains of Beijing have built a Potemkin Village. But they actually believe its real because they do not have even a passing acquaintanceship with the requisites and routines of a real capitalist economy.

Ever since the aging oligarch(s) who run China were delivered from Mao’s hideous dystopia by Mr. Deng’s chance discovery of printing press prosperity, they have lived in an ever expanding bubble that is so economically unreal that it would make the Truman Show envious. Any rulers with even a modicum of economic literacy would have recognized long ago that the Chinese economy is booby-trapped everywhere with waste, excess and unsustainability.

That is, the Red Ponzi is not indicative of a just a giddy boom; its evidence of a system that has gone mad digging, hauling, staging and constructing because there was unlimited credit available to finance the outpouring of China’s runaway construction machine. The fact that China consumed more cement in three years than did the US during the entire 20th Century is just one indicator of its madcap excess.

The point is that the great paving and construction tsunami did not happen in a vacuum. All that cement consumption required the production of hundreds of thousands of cement trucks, for example, which in turned required the fabrication of of truck mounted cement mixers in even greater numbers.

But when China’s frenzy of pyramid building finally slowed—–to say nothing of stopped—here is what was left behind. That is, a vast empty cement mixer factory with unfinished product at far as the eye can see.

Old fashioned free market economists used to call that malinvestment. Yes, it is.

Empty factories like the above—–and China is crawling with them—–are a screaming marker of an economic doomsday machine. They bespeak an inherently unsustainable and unstable simulacrum of capitalism where the purpose of credit is to fund state mandated GDP quota’s, not finance efficient investments with calculable risks and returns. The relentless growth of its aluminum production is just one more example.

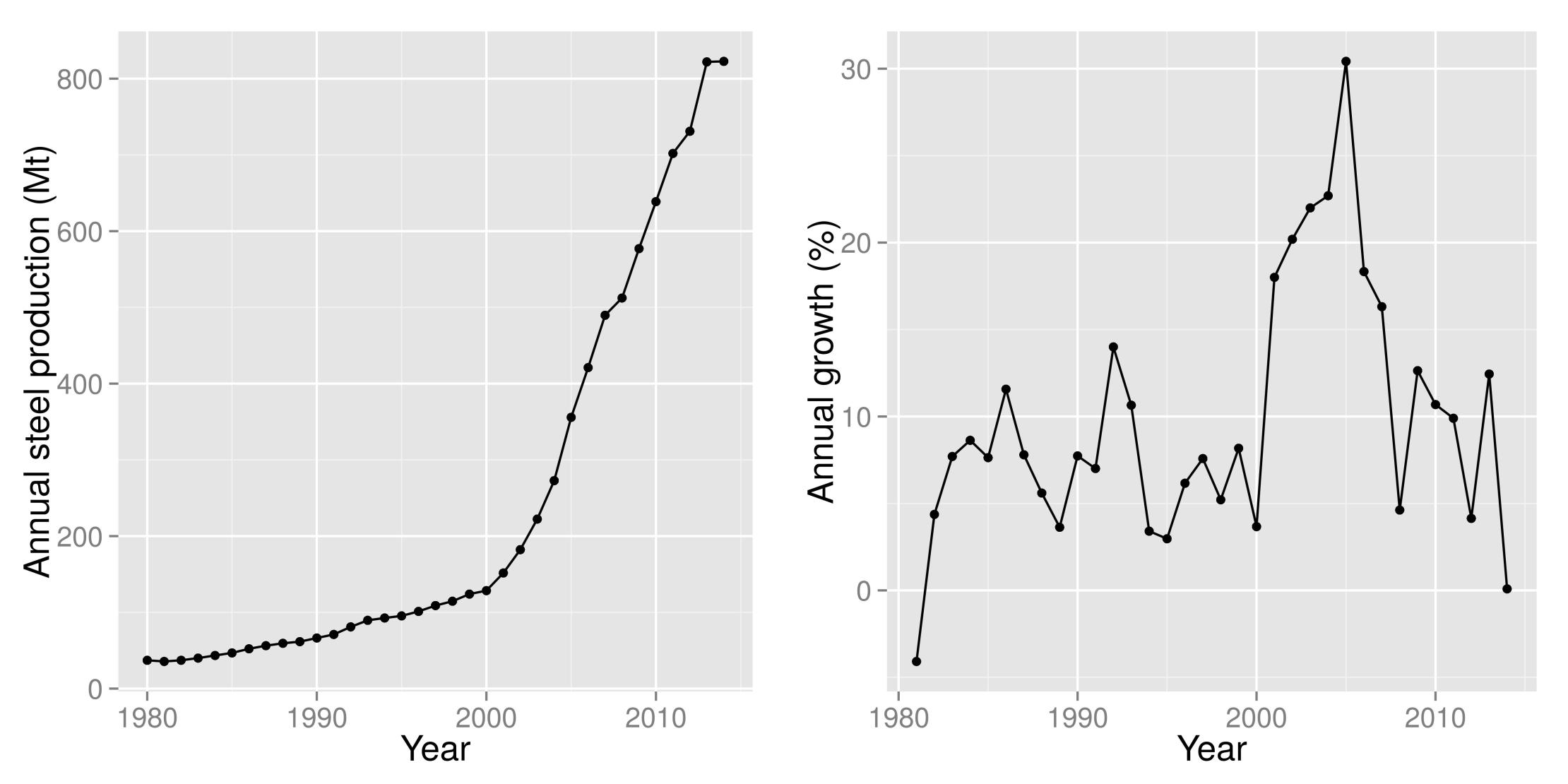

But the mother of all malinvestments sprang up in China’s steel industry. From about 70 million tons of production in the early 1990s, it exploded to 825 million tons in 2014. Beyond that, it is the capacity build-out behind the chart below which tells the full story.

To wit, Beijing’s tsunami of cheap credit enabled China’s state-owned steel companies to build new capacity at an even more fevered pace than the breakneck growth of annual production. Consequently, annual crude steel capacity now stands at nearly 1.2 billion tons, and nearly all of that capacity—-about 65% of the world total—— was built in the last ten years.

Needless to say, it’s a sheer impossibility to expand efficiently the heaviest of heavy industries by 17X in a quarter century.

This means that China’s aberrationally massive steel industry expansion created a significant increment of demand for its own products. That is, plate, structural and other steel shapes that go into blast furnaces, BOF works, rolling mills, fabrication plants, iron ore loading and storage facilities, as well as into plate and other steel products for shipyards where new bulk carriers were built and into the massive equipment and infrastructure used at the iron ore mines and ports.

That is to say, the Chinese steel industry has been chasing its own tail, but the merry-go-round has now stopped. For the first time in three decades, steel production in 2015 was down 2-3% from 2014’s peak of 825 million tons and is projected to drop to 750 million tons next year, even by the lights of the China miracle believers.

The fact is, China will be lucky to have 500 million tons of true sell-through demand—-that is, on-going domestic demand for sheet steel to go into cars and appliances and for rebar and structural steel to be used in replacement construction once the current one-time building binge finally expires.

For instance, China’s vaunted auto industry uses only 45 million tons of steel per year, and consumer appliances consume far less. So its difficult to see how China will ever have steady-state demand for even 500 million tons annually, yet that’s just 40% of its massive capacity investment.

And it is also evident that it will not be in a position to dump its massive surplus on the rest of the world. Already trade barriers against last year’s 110 million tons of exports are being thrown up in Europe, North America, Japan and nearly everywhere else.

This not only means that China has upwards of a half-billion tons of excess capacity that will crush prices and profits, but, more importantly, that the one-time steel demand for steel industry CapEx is over and done. And that means shipyards and mining equipment, too.

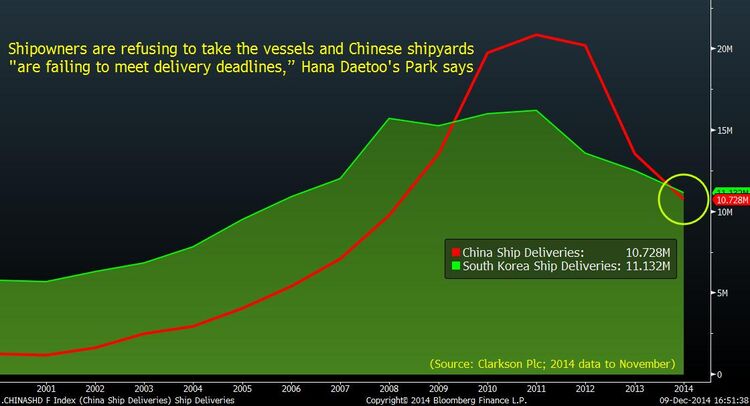

That is already evident in the vanishing order book for China’s giant shipbuilding industry. The latter is focussed almost exclusively on dry bulk carriers——-the very capital item that delivered into China’s vast industrial maw the massive tonnages of iron ore, coking coal and other raw materials. But within in a year or two most of China’s shipyards will be closed as its backlog rapidly vanishes under a crushing surplus of dry bulk capacity that has no precedent, and which has driven the Baltic shipping rate index to historic lows.

Accordingly, the outward forms of capitalism are belied by the substance of statist control and central planning. For example, there is no legitimate banking system in China—just giant state bureaus which are effectively run by party operatives.

Their modus operandi amounts to parceling out quotas for national GDP and credit growth from the top, and then water-falling them down a vast chain of command to the counties, townships and villages below. There have never been any legitimate financial prices in China—all interest rates and FX rates have been pegged and regulated to the decimal point; nor has there ever been any honest financial accounting either—-loans have been perpetual options to extend and pretend.

Thus, we now have the absurdity of China’s state shipping company (Cosco) ordering 11 massive containerships that it can’t possibly need (China’s year-to-date exports are down 20%) in order to keep its vastly overbuilt shipyards in new orders. And those wasteful new orders, in turn will take plate from China’s white elephant steel mills:

This and other state-owned shipyards are being kept busy by China Ocean Shipping Group, better known as Cosco, the country’s largest shipper by carrying capacity, which ordered 11 huge container ships last year. Caixin, the financial magazine, reported that the three ships ordered from Waigaoqiao would be able to carry 20,000 20ft containers, making them the world’s largest.

The weakening yuan and China’s waning appetite for raw materials have come around to bite the country’s shipbuilders, raising the odds that more shipyards will soon be shuttered.

About 140 yards in the world’s second-biggest shipbuilding nation have gone out of business since 2010, and more are expected to close in the next two years after only 69 won orders for vessels last year, JPMorgan Chase & Co. analysts Sokje Lee and Minsung Lee wrote in a Jan. 6 report. That compares with 126 shipyards that fielded orders in 2014 and 147 in 2013.

Total orders at Chinese shipyards tumbled 59 percent in the first 11 months of 2015, according to data released Dec. 15 by the China Association of the National Shipbuilding Industry. Builders have sought government support as excess vessel capacity drives down shipping rates and prompts customers to cancel contracts. Zhoushan Wuzhou Ship Repairing & Building Co. last month became the first state-owned shipbuilder to go bankrupt in a decade.

It is not surprising that China’s massive shipbuilding industry is in distress and that it is attempting to export its troubles to the rest of the world. Yet subsidizing new builds will eventually add more downward pressure to global shipping rates—-rates which are already at all time lows. And as the world’s shipping companies are driven into insolvency, they will take the European banks which have financed them down the drink, as well.

Still, the fact that China is exporting yet another downward deflationary spiral to the world economy is not at all surprising. After all, China’s shipbuilding output rose by 11X in 10 years!

Folks, this doesn’t happen in a world anchored in economic sanity.

But there is a larger picture. This is not just an “economic trainwreck in one country”, to paraphrase the edict of Joseph Stalin, that doesn’t matter to the rest of the world.

The astonishing foolishness of the Beijing regime has now become a clear and present danger to the entire global economy. It is a veritable fount of deflationary tidal waves that are being exported to the rest of the world and which are bringing about a global CapEx depression and a thundering collapse of profits throughout the global chain of industrial production.

As Donald Trump speeds toward the White House, the mainstream media will soon be gumming vigorously about how American politics became so unhinged.

They need look no further than the Red Suzerains of Beijing. It is their monumental foolishness that has made The Donald possible.

![]()

Запись The World Economy Wreckers Of Beijing впервые появилась crude-oil.top.