Submitted by David Stockman via Contra Corner blog,

Mario had a bee in his bonnet yesterday morning. Apparently, the chorus of German voices pointing to the obvious—- that his policies are killing savers, insurance companies, pension funds and banks—-got his dander up:

“We have a mandate to preserve price stability for the whole of the euro zone, not only for Germany,” he said. “We obey the law, not the politicians, because we are independent.”

There you have in brief the whole rationalization for the monetary madness that Draghi and his kindred central bankers have unleashed on the world. They claim that their rubbery statutory mandates to pursue the equivalent of economic apple pie, such as ‘price stability’, leads in a straight, unbreakable line of logic and monetary science to the lunacy of negative 0.4% money market rates and $90 billion per month of bond-buying.

No it doesn’t. There is no scientific linkage whatsoever—–just an ideological leap based on a Keynesian demand model that conveniently delegates all power to the central bankers’ soviets.

Just as in the case of the Humphrey-Hawkins Act in the US, the ECB’s enabling statute does not define price stability in quantitative terms—-nor does it specify the inflation index to be used or the duration to be measured. Even when the ECB’s Governing Council attempted to formulate a quantitative definition of ‘price stability’, it only got slightly more specific in defining it as something between zero and 2% over the course of a year.

“Price stability is defined as a year-on-year increase in the Harmonised Index of Consumer Prices (HICP) for the euro area of below 2%.”

By its own definition, therefore, the eurozone does not have a “deflation” problem or even a “lowflation” threat. For the last 16 years, the core HICP has averaged 1.5%, and during the last year when allegedly the deflationary sky was falling, the core consumer inflation index has risen by 1.0%.

So all of Draghi’s arm-waving about the “law” is just risible obfuscation. Surely “Mario and the NIRPs” are not suggesting that monetary policies so radical that they were not even conceivable a decade ago are warranted because core inflation is temporarily tracking at a mere 50 bps below its long-term trend; or that it should be measured in weeks and months, not a year or more; or that the ECB should be fighting the huge blessing to EU consumers of the globally originated collapse in imported oil and materials inflation.

Indeed, the truth is real simple. Virtually all of the sub-trend performance of the consumer price index during the last year is due to the nearly 3% drop in import prices. And that has been an unequivocal benefit to the European economy!

So not only was Mario pouting because the phony threat of deflation has not blinded the Germans to the destructive impact of his policies, but he actually let loose a wild pitch that needs no amplification. To wit, Draghi is on a power trip so naked that he actually threatened even greater monetary mayhem if people don’t stop questioning his authority:

“Any time the credibility of a central bank is perceived as being put into question, the result is a delay in the achievement of its objectives — and therefore the need for more expansion,” the ECB president told reporters in Frankfurt, raising his voice. “Our policies work, they are effective. Just give them time.”

There you have it—–school yard bluster. And its all in the name of a primitive economic notion that only someone nurtured in the Italian Treasury and sent off to finishing school at Goldman Sachs could actually believe. To wit, that more debt everywhere and always is the elixir that will create economic growth and wealth.

In fact, Mario believes himself to be in the economic growth business via the agency of pumping more credit into the eurozone economy whether warranted or not. Apparently, there are no interest rates too low if they spur more credit growth:

“Our monetary-policy measures have been supporting growth……. With rare exceptions, monetary policy has been the only policy in the last four years to support growth………Overall, the monetary policy measures in place since June 2014 have clearly improved borrowing conditions for firms and households, as well as credit flows across the euro area…….Credit continues, it’s pretty solid,” he said. “Together with a dramatic fall in rates and increasing volumes, this shows are measures are indeed quite effective.”

Let’s see. Private sector loans outstanding in the eurozone totaled EUR 10.69 trillion in February compared to EUR 10.60 trillion a year earlier. That computes to a gain of exactly……..0.6%!

Put differently, when you are not counting angels on the head of a pin you rarely see one. So it is not surprising that Mario is seeing the debt elixir at work where the statistics show hardly a shadow:

Broad financing conditions in the euro area have improved. The pass-through of the monetary policy stimulus to firms and households, notably through the banking system, is strengthening…..Bank credit has been going up since second quarter of 2014. Rejections have been going down. This shows that our measures have indeed been most effective.”

So even if European households and businesses needed to lug around more debt, which they clearly don’t, the ECB has literally savaged savers and pensioners in the name of a hardly measureable fraction.

Obviously, there is an altogether different issue here. The European private sector is not borrowing because interest rates were too high two years ago when QE incepted, or even four years ago when Draghi delivered his “whatever it takes” ukase.

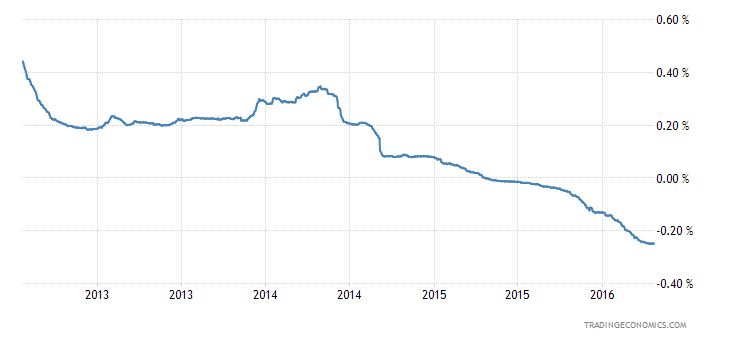

In fact, since mid-2012 euro LIBOR has essentially been pegged at a rounding error. The notion that the difference between +0.2% on the lending reference rate and -0.2% matters to any actual business or household is preposterous.

The fact is, lending growth is tepid because the eurozone private sector is impaled on Peak Debt. The boom in lending happened 7-15 years ago. And even after plateauing at Peak Debt, the growth rate since the year 2000 still computes to 5% per annum.

So there is another reason why Europe isn’t growing and its one the central bank can do nothing about. Namely, the 19 governments of the eurozone and the super-state in Brussels have essentially outlawed it. If you want to know why growth is so tepid just examine the eurozone’s massive barriers to enterprise and work in the form of taxes, regulation, welfare state extravagance, crony capitalist subsidies and privileges and labor law protectionism.

In a word, the problem is not that private sector credit is too niggardly; it’s that the leviathan state has crushed the ingredients of supply side enterprise and growth. When the state budget consumes 50% of GDP, and its tentacles of regulation and intrusion penetrate most of the rest, the central bank’s printing press is impotent.

Nevertheless, when your only tool is a hammer, everything does look like a nail. So Draghi and the NIRPs will undoubtedly keep on printing until they blow the euro-based financial markets sky high.

That the testy Italian is clueless about the massive bond market bubble his policies are creating was starkly evident in another gem from today’s presser. Mario’s message to the Germans was to suck it up and that he doesn’t have anything to do with low rates anyway:

It is clear that pension funds and others, insurance companies, are seriously affected by the low interest rates – I would caution them not to blame on low rates everything that has gone wrong in the sector – but they are seriously affected……Low interest rates are a symptom of low growth and low inflation. If we want to return to higher interest rates we need to return to higher growth and higher inflation. …

Does this blithering fool believe he has repealed the law of supply and demand? That the ECB can plunge into the European bond market to the tune of $90 billion per month and not impact the price of debt?

Worse still, does he not recognize that the ECB massive intrusion into the bond market has also triggered second order dynamics that drastically amplify this artificial bid? To wit, the bond vigilantes of yore have become today’s repo financed front-runners, piling into everything today that Mario and the NIRPs will be buying tomorrow.

As of two days ago, the German 10-year bund was trading at a 13 bps yield and the Italian bond at 140 basis points. Neither of these rates make a wit of economic sense, and most surely they are not owing to “low growth”.

Instead, their prices have been driving into the financial stratosphere by the ECB’s big fat bid and the front runners’ scramble to scoop-up the unspeakable windfall gains that clueless Mario has bestowed on the casino.

Likewise, has Draghi not noticed that while bank loans to households and operating businesses have barely blipped upwards there has been an explosion of high yield bond issuance? Never mind that almost to the last euro the proceeds have been used to fund M&A rollups, buyouts and other financial engineering schemes, not an expansion of productive assets.

But here’s the thing. The world’s greatest monetary charlatan is nearly out of tricks. He pointedly backed off from helicopter money yesterday because the Germans have obviously drawn a line in the sand. And he can’t push NIRP much further without breaking what remains of Europe’s sclerotic socialist banking system. And if he tries even more negative carry money under TLTRO it will assuage the margin pressure on European banks but not make the eurozone’s debt besotted households and businesses a wit more credit-worthy or inclined to borrow.

So this foolishly naïve believer in the elixir of debt is actually pushing on a credit string while inflating the mother of all bond bubbles. There is not a chance that the ECB can extract itself from this dangerous corner, nor continue down the current path much longer.

Indeed, when the casino front runners finally conclude that the Draghi jig is up, the European bond market will plunge into a bidless pit as they race to cash in their capital gains and liquidate their repo borrowings.

Then there will be a whole hive of angry bees in Draghi’s bonnet, German speaking ones in the lead.

The post The World’s Greatest Monetary Charlatan Is Nearly Out Of Tricks appeared first on crude-oil.top.